| Goldco boasts 5M oz. gold, C$1B in NPV | | | Please find below a special message from our advertising sponsor, KORE Mining. Golden Opportunities is a free service that gives you valuable investment intelligence all year long at no charge, and advertisements allow us to continue sending these reports. | |

What would you call a company with nearly 5 million ounces of gold and two projects potentially worth a combined C$1 billion?

You’d call it KORE Mining (KORE.V; KOREF.OTC), a bargain-priced, gold-focused junior with tons of established value, an uber-clean share structure and lots of room to grow.

| | |

What would make the perfect gold story?

|

While such a junior mining company would always be somewhat in the eye of the beholder, the ideal company would boast definite characteristics in the current market:

|

• In situ gold: Ideally, a great gold story would have substantial ounces in the ground, with bonus points if the company has more than one project with a million-ounce resource.

• Compelling economics: The company would have at least one project with substantial after-tax net present value and rich project economics.

• District-scale potential: Exploration upside that gives the company a major growth angle to complement development-stage deposits. Again, bonus points accrue if the projects in question are in safe mining jurisdictions.

• A clean share structure: A tightly-held structure where management has significant skin in the game that aligns management’s goals with shareholders.

• Significant undervaluation: To maximize leverage, invest in companies where the market isn’t giving the company anywhere near full credit for its inherent value relative to its peers

|

As it happens, KORE Mining (KORE.V; KOREF.OTC) fits this description to a tee.

And with the gold market set to ride fiscal and monetary stimulus higher in the year ahead, KORE is sitting on one of the sector’s most attractive project portfolios and has a clear strategy to leverage the yellow metal’s next big uptick.

|

A Near Five-Million-Ounce Head Start

|

It starts with those in situ ounces.

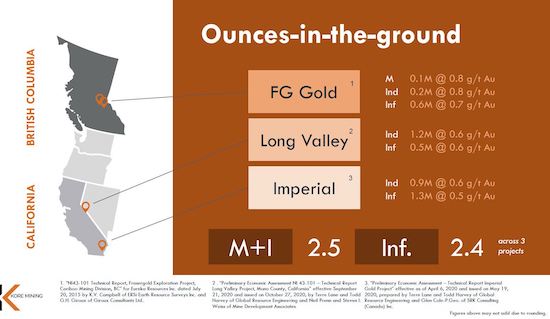

Between its Imperial and Long Valley projects in California and its FG Gold project in British Columbia, KORE has a global gold resource of almost five million ounces.

That hefty total includes a 2.2-million-ounce resource at Imperial, a 1.7-million-ounce resource at Long Valley and a near-million-ounce resource at FG Gold.

The graphic below breaks the numbers down into their respective confidence levels.

| |

|

As you can see, the measured and indicated resource for these three projects is 2.5 million ounces and the inferred resource is 2.4 million ounces.

In a time of rising gold prices, all by itself, this global resource of open-pittable gold projects in safe mining jurisdictions makes KORE a fantastic optionality play.

But there’s more to the KORE story than optionality. Much more.

Save

Not A Subscriber Yet?

Get Golden Opportunities For Free

Subscribe to our Golden Opportunities e-letter to receive timely market

updates from the Gold Newsletter research team, plus video

presentations by expert speakers from the New Orleans Conference

— and the Investor’s Guide to Gold and Silver — all at no cost!

CLICK HERE to start your subscription.

|

Development-Stage Projects With Over C$1 Billion In NPV

|

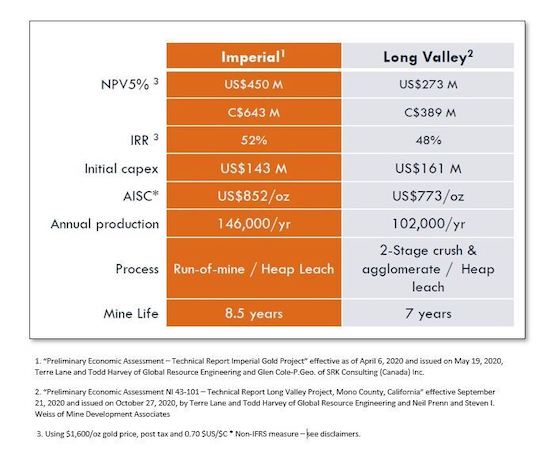

You see, KORE has produced preliminary economic assessments for both Imperial and Long Valley.

Both boast great economics, with Imperial having a post-tax net present value, discounted at 5% of C$643 million, and Long Valley having a C$389-million, 5%-discounted, after-tax NPV. Both forecasts assume a US$1,600/oz. gold price.

You read that right. Together, these highly profitable assets have a combined net present value of C$1 billion…and KORE Mining currently sports just a C$150 million market cap.

| |

|

And these development-stage projects have more than just the leverage power of great top-line valuation numbers going for them.

They’re also attractive from a potential acquirer’s perspective because they feature affordable initial capex numbers.

In fact, Imperial, KORE’s most advanced project, would require an initial capital outlay of just US$143 million (or less than a third of its projected post-tax NPV in U.S. dollars).

Both Imperial and Long Valley are open-pittable and heap-leachable, which makes them appealing to producers, especially given their relatively low all-in sustaining production costs.

|

In other words, without adding another ounce of gold to its global resource total, KORE already has two tempting acquisition targets.

|

But with the district-scale potential of Imperial, Long Valley and FG Gold, growth via the drill bit is highly likely.

| |

Thanks to a couple of recently closed private placements led by mining legend (and company kingmaker) Eric Sprott, KORE has C$10 million in the bank to pursue drilling and exploration to expand its three key projects.

| |

|

At FG Gold, the drills are turning as we speak to both improve the grades on the existing resource and extend those resources at depth.

Plus, FG Gold has a staggering 100 kilometers of potential trend that KORE could test on the project, making new discoveries a distinct possibility.

At Long Valley meanwhile, a drill program will begin next year to test a series of near-surface oxide targets and for the possibility of high-grade feeder structures at depth.

At Imperial, which lies adjacent to the long-lived (and profitable) Mesquite mine, KORE has more than 28 kilometers of trend to test, with multiple targets that could expand Imperial’s two-million-ounce-plus resource. Initial surface results are due soon.

Long-term, the potential to add millions more ounces via drilling to KORE’s five-million-ounce total gives the company growth upside to go with its development-stage assets.

|

Undervalued With Share Price Catalysts Galore

|

Based on companies with comparable assets, KORE Mining is an exceptional bargain.

On a market cap-per-ounce basis, it’s trading at US$22/oz. — while peers are trading at two to three times those levels.

On a Price/Net Asset Value basis, the story is the same, with KORE’s C$150 million market cap implying a P/NAV of ~0.2x, or roughly a quarter of the average level of its peers.

|

With drilling at FG Gold turning out encouraging assays on a regular basis for the next few months — and the program to test targets at Imperial started — KORE won’t lack for news flow.

|

That uber-clean share structure promises a significant re-rating on good news on either the exploration or development fronts for its projects.

As higher gold prices attract more generalist investors to this sector, KORE’s C$1 billion of combined NPV and exploration upside should attract them like moths to a flame.

That’s why it’s so critical to look at KORE Mining now, before the rest of the market finds its way to this near-perfect gold story.

| | | You are receiving this message because you have specifically subscribed to Golden Opportunities, have purchased a product or have registered for a conference with us or with one of our partners. If you'd rather not receive emails from us, please unsubscribe here. Remember, your personal information will never be rented or sold and you may unsubscribe at any time. Advertisements included in this issue do not constitute endorsements from us of any stock or investment recommendation made by our advertisers.

Warnings and Disclaimers: As you know, every investment entails risk. Golden Opportunities hasn’t researched and cannot assess the suitability of any investments mentioned or advertised by our advertisers. We recommend you conduct your own due diligence and consult with your financial adviser before entering into any type of financial investment. This profile should be viewed as a paid advertisement. The publisher and staff

of this publication may hold positions in the securities of companies discussed or recommended. The information contained herein has been received from sources which the publisher deems reliable. However, the publisher cannot guarantee that such information is complete and true in all respects. The advertiser provided a review of the factual content of this advertisement at the time of publication. The publisher

is not a registered investment adviser and does not purport to offer personalized investment related advice; the publisher does not determine the suitability of advice and recommendations contained herein for any reader. Each person must separately determine whether such advice and recommendations are suitable and whether they fit within such person’s goals and portfolio. The advertiser featured in this edition of Golden

Opportunities has paid the publisher for the costs and compensation related to the authorship, overhead, design and distributing this online edition, in the amount of $7,500. The publisher may receive revenue, the amount of which cannot be predetermined, from sales resulting from any accompanying offer. Authors of articles contained herein may have been compensated for their services in preparing such articles.

Golden Opportunities

Jefferson Companies

111 Veterans Memorial Blvd. Suite 1555

New Orleans, LA 70118

1-800-648-8411

| | | |

.png)