Even in the midst of new variants and case count surges, the world is clearly gearing up for a big economic rebound.

|

With people buying cars in a Covid-related shift away from public transportation — and busting at the seams to travel — the peak summer season could see oil improve on the already impressive bounceback into the $60s we’ve seen in recent months.

|

It’s a confluence of events that plays right into Hemisphere Energy’s (HME.V; HMENF.OTC) hands.

|

As you’re about to see, Hemisphere’s Atlee Buffalo project in southeast Alberta gives it a cash-flowing asset with a growing production profile and a proven path to boost yield.

And yet this company also offers one of the most compelling valuation mismatches in the sector.

In an investment space where only a handful of names have survived a long bear-market shakeout, Hemisphere Energy stands out as a potent lever on a return to normalcy.

|

The Cash Is Flowing & Growing

|

One of the benefits of that “survival of the fittest” dynamic in the explorer-developer end of the oil and gas space is that the surviving companies tend to be cash-flow positive.

That’s certainly the case with Hemisphere Energy.

The heavy oil pools it is tapping at Atlee Buffalo are set to produce C$19 million in adjusted funds flow from operations in 2021 — and C$30 million in 2022.

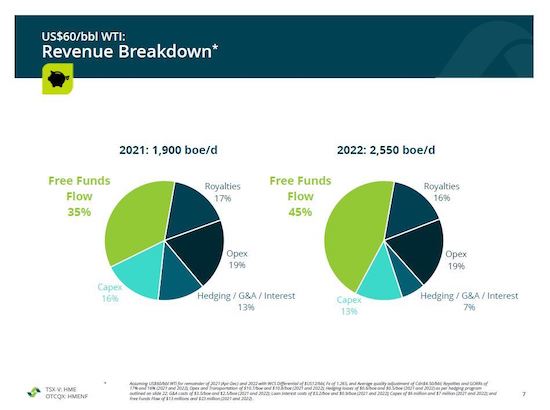

As the chart below shows, an increase in free funds flow will coincide with an increase in average annual production from 1,900 boe/day to 2,550 boe/day.

|

|

|

| Hemisphere’s already robust free funds flow percentage is set to grow. |

In 2022, free funds flow as a percentage of overall revenues will improve to 45%, from 35% this year.

At that cash flow growth rate, management expects to exit 2021 with its net debt cut in half, and they expect to exit 2022 with a C$9 million net cash position.

|

In Progress:

A Proven Method To Increase Yield

|

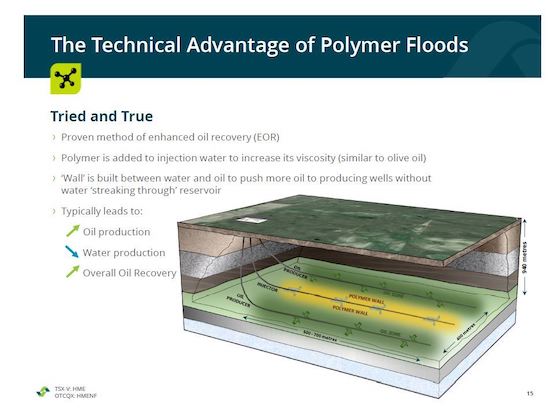

Hemisphere has built its production and cash flow growth forecasts on the ability of “polymer flooding” to increase the yield of Atlee Buffalo’s oil pools.

This process involves injecting a polymer roughly the viscosity of olive oil into horizontal wells within the reservoir. The pressure from the resulting polymer wall helps push more oil to the surface.

|

|

|

| Polymer flooding project promises to increase Hemisphere’s oil pool yields. |

This is a proven technology used by heavy oil producers globally, and with only 5% recovery made of the project’s reserves to date, a soon-to-complete polymer flood conversion on its G pool reservoir should accelerate both recoveries and production.

|

It’s a low-risk, high-reward method that promises to improve production this year on the G pool and next year on the F pool.

|

It also has the virtue of keeping Atlee Buffalo’s environmental footprint small, an important selling point for local stakeholders.

Save

Not A Subscriber Yet?

Get Golden Opportunities For Free

Subscribe to our Golden Opportunities e-letter to receive timely market

updates from the Gold Newsletter research team, plus video

presentations by expert speakers from the New Orleans Conference

— and the Investor’s Guide to Gold and Silver — all at no cost!

CLICK HERE to start your subscription.

|

Severely Undervalued Relative To Peers

|

More importantly from our perspective as investors, however, is the valuation disconnect currently occurring with Hemisphere Energy’s market cap.

This is a company currently trading at around C$40 million.

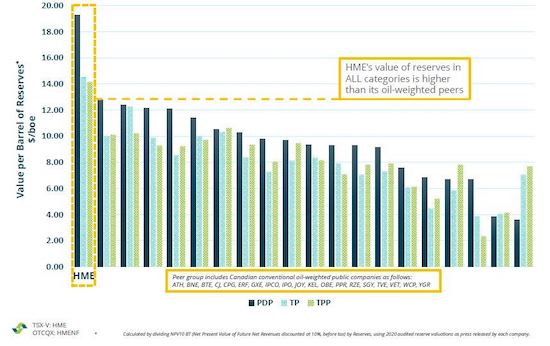

This is true despite the fact that, as the chart below shows, HME stands head and shoulders above its oil-weighted peers in terms of the value of Atlee Buffalo’s reserves.

|

|

|

| HME’s reserve value stands head-and-shoulders above its peers… |

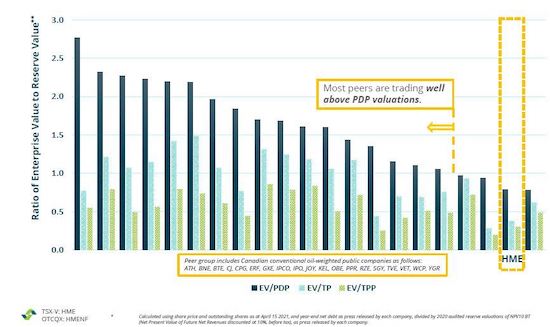

Yet, amazingly, per this next chart comparing its enterprise value to reserve value ratio, Hemisphere boasts a valuation mismatch that’s practically begging to be corrected.

|

|

|

| …and yet HME remains severely undervalued on an EV-to-RV basis. |

Even a modest move to the middle of the pack on this valuation metric would give those who build a position in HME at current levels an easy double on their investment.

|

A Nearly Uncapped Upside…

But Your Window Of Opportunity Is Closing

|

And that’s just the table stakes.

Because that potential doubling assumes a trading level roughly equal to a C$81 million estimate of Hemisphere’s “proved developed producing” (PDP) reserves, the most conservative of the reserve estimates.

|

But the third-party auditor that generated that estimate also valued Atlee Buffalo’s proved reserves at C$170 million and its proved and probable reserves at C$211 million.

|

You read that right.

In the hot oil market that seems likely around the corner, Hemisphere Energy could easily see its value shift towards these more optimistic estimates.

It’s a possibility that could see the company’s market cap increase much, much more from current levels.

|

That degree of leverage simply isn’t possible when you invest in oil and gas multinationals…and it’s what makes Hemisphere Energy such a smart-money buy right now.

|

With an upside that’s nearly uncapped and broader market trends moving very much in its direction, Hemisphere Energy is a name you’ll want to look at now to maximize your gains in the post-Covid economy.

|

.png)