The junior mining market is remarkably inefficient.

|

That’s not a bad thing. In fact, it’s a great thing for investors who by good luck or hard work can uncover the gems left behind by the market’s quickly shifting attention.

|

That’s precisely what seems to have happened with a company called Galane Gold (GG.V; GGGOF.OTC).

|

Already known for a multi-million-ounce gold resource and steep production growth by ramping up production on its Galaxy asset in South Africa and adding its operating Mupane mine in Botswana, Galane stunned the market this past spring when it announced the acquisition of a turnkey gold-silver mine in New Mexico.

The company’s market value spiked on the announcement, but with all the volatility in metals prices, the share price drifted back below where it was before the announcement.

Then investors seemed to be looking the other way when Galane recently announced the closing of the acquisition.

But now that they’re setting about growing their production from their existing projects and jump-starting profitable production in the U.S….the company will soon be impossible to ignore.

|

A Transformational Acquisition

|

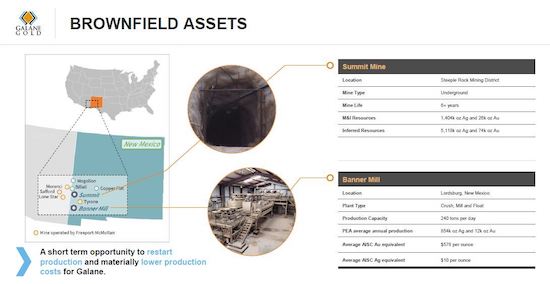

By acquiring the Summit mine and nearby Banner mill in New Mexico, Galane now has access to a brownfields project with a great chance to go into production quickly…and to grow via exploration.

|

| |

Galane has bought Summit and Banner from Pyramid Peak Mining, a wholly owned subsidiary of Waterton Global Resource Management.

Summit operated as a high-grade underground mine between 2008 and 2013, before falling precious metals prices and a profit-restricting streaming deal forced the mine to go on care and maintenance.

Waterton took over the operation in 2016 and spent US$55 million removing the streaming contract and paying off existing creditors.

Galane’s purchase price for Summit and Banner consists of total consideration of US$17 million, including US$6 million in cash on closing, US$8.2 million of cash upon hitting production milestones, share consideration of 16 million shares of Galane at C$0.22 per share and 16 million, three-year-expiry warrants priced at C$0.30.

|

That’s just under 20% of the project’s forecasted pre-tax net present value of US$97 million.

|

In short, this has all the markings of a very accretive deal for Galane.

|

A Clear Path To Production Profits

|

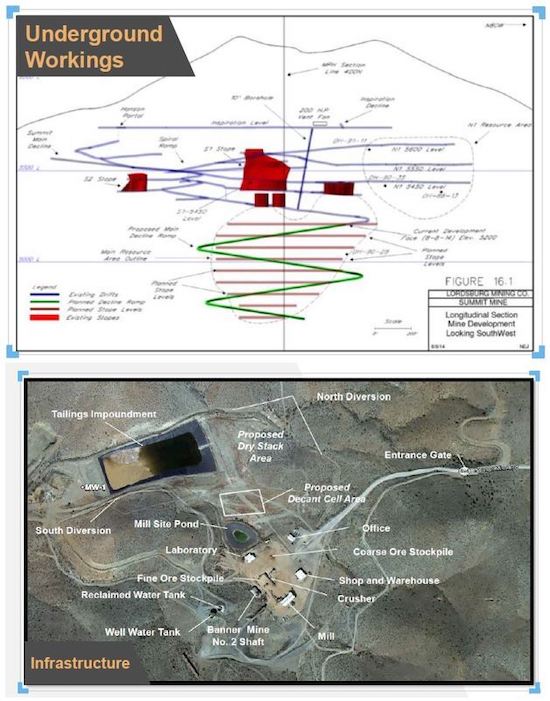

Better still, as you can see from the following images, Summit has practically everything it needs to get into production.

|

| |

That includes an NI 43-101 compliant resource, 15,000 feet of underground infrastructure…and the Banner mill just 57 kilometers away to process Summit’s ore.

Summit contains an indicated resource of 1.4 million ounces silver and about 25,000 ounces gold, plus an inferred resource of 5.1 million ounces silver and approximately 74,000 ounces gold.

The mine also sits within easy road distance from Tucson, Arizona and has a tailings area, an on-site water tank, a shop and a mill.

Plus, thanks to Waterton, it has all the permits in place to quickly restart production.

Save

Not A Subscriber Yet?

Get Golden Opportunities For Free

Subscribe to our Golden Opportunities e-letter to receive timely market

updates from the Gold Newsletter research team, plus video

presentations by expert speakers from the New Orleans Conference

— and the Investor’s Guide to Gold and Silver — all at no cost!

CLICK HERE to start your subscription.

|

Obvious Exploration Upside

|

For a company that wants to begin mining Summit in short order, those in-place items give Galane a massive head start.

|

And that head start is indeed just the start — because the resource has a great chance to grow significantly from here.

|

First, past work indicates that there’s mineralization above and below the existing resource and workings at Summit. This is low-hanging fruit that Galane can begin testing immediately as it ramps up production there.

Then there is the Billali zone, which is located northwest of Summit and has generated historical surface evidence that suggests it could host still more mineralization.

Consider that the area was last drilled in the early 1990s and yielded assays of up to 681.3 g/t silver and 9.4 g/t gold over 4.4 meters.

Finally, there’s a 2,000-foot-long IP anomaly on the Mohawk area next to Billali that’s generated high-grade silver and gold assays of its own.

|

Because the owners pre-Waterton were undercapitalized, that group never engaged in extensive exploration to follow up on these targets after 1992.

|

With the cash flow that should be coming in soon from Summit, Galane could have the resources to start testing these targets extensively.

|

|

The team at Galane is uniquely qualified to get Summit re-started.

It has already done so at Mupane and is in the process of ramping to commercial production at Galaxy.

|

| |

With the addition of Summit, the path is clear to make a quick and profitable addition to that production…and with a silver component to boot.

Here’s the key: Galane is already known for its multi-million-ounce resource and steep production profile in Africa.

|

Now the company has acquired significant gold-silver production assets in the U.S….and the market seems to be completely overlooking this transformational development.

|

As the company itself puts it, Galane is “a gold producer with management and assets in place to triple production and materially lower production costs.”

Relatively few mining investors have yet discovered this fact. Now you have.

Bargain-priced (for now) at current trading levels, this company has the potential to surprise the market by quickly flipping the switch on production at Summit.

If you’re bullish on gold and silver, you’ll want to take a closer look at Galane Gold.

|

|

.png)