Potential valuation mismatches don’t come much starker than this one.

|

Tiny Altair Resources (AVX.V; AAEEF.OTC) has taken the junior gold sector by storm over the past few months by announcing not one, but two company-making deals.

|

Taken individually, each of these deals argues for a substantial re-rating of Altair’s share price.

Together, they create one of the most compelling (and overlooked) stories in the gold space today.

|

With an advanced-stage exploration project in Burkina Faso and a deal in the due diligence phase for in-production assets in Kazakhstan, Altair is quietly building a solid foundation for a multi-mine gold producer and at the same time is putting together a potent lever on rising gold prices.

|

Securing A Million-Ounce-Plus

Project In Burkina Faso

|

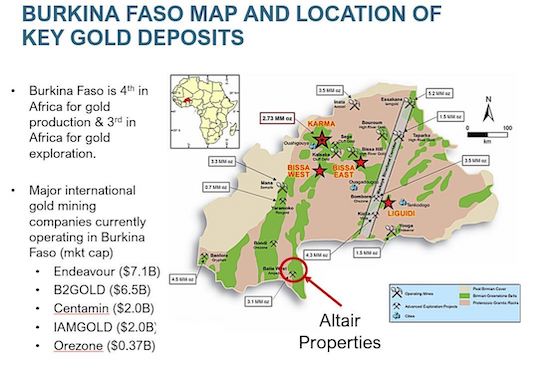

The acquisition fireworks started for Altair in June, when the company announced the acquisition of an open-pit gold project in Burkina Faso’s southwest corner.

The country is a hot gold jurisdiction, a key player within the West Africa region that produced more than 11 million ounces of gold in 2020.

|

| |

| Altair just acquired an advanced-stage project in Burkina Faso, part of a West Africa region that produced more than 11 million ounces of gold in 2020. |

Several major gold mining companies currently operate in Burkina Faso, and the Marbera 2 permit that covers Altair’s three concessions lies within 50 kilometers of 10 million ounces of gold resources.

Prior operators have outlined 1.3 million ounces of gold on Marbera 2, and while Altair will have to do a bit of work to bring them into compliance with Canadian regulatory standards, it’s clear the company won’t be starting from scratch here.

All three deposits on the project are open in all directions and at depth, and they come with around 100,000 meters of partially analyzed diamond drill core that will guide Altair’s exploration efforts.

|

A Play For Active

Gold Mines In Central Asia

|

Clearly, most gold juniors could hang their hats on Marbera 2 as their flagship project.

|

But in terms of company-making deals, Altair was just getting warmed up.

|

In July it announced a binding agreement to acquire two gold-producing properties in eastern and central Kazakhstan.

Talk about going from 0 to 60 — it can take years for a junior gold company to make the jump from exploration to production.

But if this deal closes as expected in early October, Altair will hit the ground running with two active mines producing about 21,000 ounces of gold per year.

|

| |

| Altair is poised to make the leap to producer, assuming its binding agreement to acquire two active gold mines in Kazakhstan closes. |

Better still, these projects contain more than two million ounces of historic resources, much of which Altair believes it can quickly pull into mine plans for these operations.

And the potential growth curve here is steep, with current operations projected to generate about 36,000 ounces annually over the next two years and to reach 120,000 ounces within four years, based on existing infrastructure. That growth in production would throw off impressive cash flow at any gold price.

With inflationary pressures near the boiling point and gold poised for a secular bull run, this deal would position Altair perfectly to convert higher gold prices into even greater cash flow.

Save

Not A Subscriber Yet?

Get Golden Opportunities For Free

Subscribe to our Golden Opportunities e-letter to receive timely market

updates from the Gold Newsletter research team, plus video

presentations by expert speakers from the New Orleans Conference

— and the Investor’s Guide to Gold and Silver — all at no cost!

CLICK HERE to start your subscription.

|

The Right Connections

To Make These Deals Happen

|

Of course, neither Altair’s Burkina Faso project nor its agreement for these Kazakhstan projects is costless.

The company is acquiring Marbera 2 for an initial US$2.3 million in cash and another US$2.0 million in cash (plus three million in shares) once Altair brings the project’s 1.3 million ounces of historic gold into NI 43-101 compliance.

The deal also has significant cash payments tied to various project and production milestones. The key, though, is that Altair has already been able to tee up a C$2.75 million private placement to cover the initial payment for Marbera 2.

|

And it is in active discussions with institutional investors to cover the US$106 million cost of the Kazakhstan deal on terms that would include debt and other means that will minimize dilution at the current share price.

|

That a company Altair’s size can attract that kind of backing tells you everything you need to know about the connections and business acumen of its management team.

|

|

More importantly for potential investors, though, is the leverage to these projects’ upside that Altair’s financial engineering can provide.

Assuming the deal for the Kazakhstan assets closes, a company with a C$6 million market cap will offer exposure to projects that could be worth many, many multiples of that valuation.

|

Take a deep dive into the junior mining sector if you want — you’ll be hard-pressed to find a stock this inexpensive with an upside this compelling.

|

This company has already taken not one, but two steps on a path that will transform it into a heavyweight in gold mining sector.

Especially if you like the long-term outlook for gold, you’ll want to start doing your own due diligence on Altair Resources now.

|

|

.png)