If recent history is any guide, gold royalty and streaming companies will be the first names off the shelf when gold makes its next big run.

|

That fact can come as a surprise to investors new to the sector, who tend to gravitate toward exploration and development plays to add leverage to their gold trade.

But while exploration-based discoveries can be a great way to make money in the space, they are often overly reliant on one or two flagship projects for success.

Development stage companies can deliver leverage too but can also get bogged down in the process of getting a mine up and running.

|

Royalty companies, by comparison, can cast their nets widely in terms of investable projects and offer accelerating cash flows when gold prices start to move.

|

And, as you’re about to see, early-stage, newly-trading Empress Royalty (EMPR.V; EMPYF.OTC) has all the upside of a pre-discovery explorer — but thanks to its royalty and streaming model, it has significant revenue and cash flow growth directly in front of it.

|

A Track Record Of

Market-Beating Performance

|

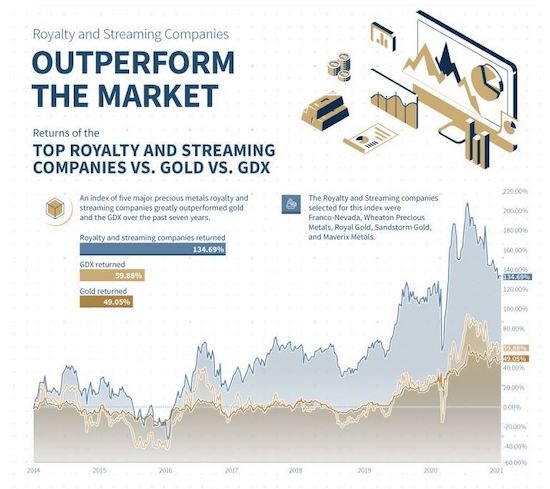

If you want an idea of the leverage potential royalty and streaming plays offer, take a look at the chart below.

|

| |

| Click image for more detail

|

The chart compares the performance of physical gold, the GDX (an ETF of gold miners) and a group of five major royalty and streaming companies.

Gold’s extended up-move began in 2019 before it made a big run in 2020, posting an average return of 49.05% since 2014. The GDX did slightly better, returning 59.88%.

That’s a solid performance, but it’s dwarfed by the leverage that those major royalty and streaming companies turned in over the same period.

|

At 134.69%, that average gain for royalty companies is a near-three-fold besting of gold’s returns.

|

As you’ll see in a moment, these impressive returns can get even better when you invest in royalty companies that are still, like Empress, in their early stages of growth.

|

|

First though, it’s worth reviewing how these companies make money.

They do this in two primary ways, through a royalty (a payment based on either a percentage of gold or silver produced at a mine or on the revenues or profits generated from the sale of a mine’s minerals) or a stream (the right to purchase a portion of one or more metals produced from a mine, at a deeply discounted price).

|

| |

| Click image for more detail

|

To acquire these investments, the royalty or streaming company provides the mine developer, operator or explorer a non-dilutive source of cash that it can use to grow an exploration-stage resource, put a mine into production or expand a mine’s operations.

Save

Not A Subscriber Yet?

Get Golden Opportunities For Free

Subscribe to our Golden Opportunities e-letter to receive timely market

updates from the Gold Newsletter research team, plus video

presentations by expert speakers from the New Orleans Conference

— and the Investor’s Guide to Gold and Silver — all at no cost!

CLICK HERE to start your subscription.

|

Partnerships Bring

Deal-Making Firepower

|

As you can imagine, the profit-potential of this model makes the competition fierce to acquire existing royalties and streams.

|

And that’s what sets Empress apart from its competitors in the sector — Empress is focused only on royalty and stream creation, not acquisition.

|

Leveraging the financial and deal-making firepower of its three partners — Endeavour Financial, Terra Capital and Accendo Banco — Empress actively seeks out developers and producers looking for non-dilutive sources of cash flow to build or expand mines.

How successful has this strategy been?

|

Consider this: Empress only listed as a public company in late 2020, and yet it already owns royalties or streams on four producing/near-production operations and another 13 on projects at the exploration stage.

|

And its deal-making pipeline is packed — the company is currently actively reviewing more than 20 projects that represent over US$100 million in potential investments.

|

|

In a sector where cash flow and revenue growth are paramount, Empress is already seeing cash flowing from its gold stream on the Sierra Antapite gold mine in Peru.

That will be followed in Q1 2022 by cash from a stream on the silver production from the Tahuehueto silver mine in Mexico, a 1% Net Smelter Return (“NSR”) royalty on the Pinos gold and silver mine (also in Mexico) and a 2.25% NSR on that Manica gold mine in Mozambique.

Based on that production schedule, Empress is forecasting revenues of approximately USD$6 million in 2022, USD$9 million in 2023 and over USD$12 million in 2024.

|

That’s a serious growth curve — and all that is before the impact of that massive deal-flow pipeline ahead for the company.

|

Add it all up, and it makes Empress Royalty stand out as arguably the most compelling early-stage bet in the royalty space.

|

A Unique Opportunity

To Get In Early

|

What’s the potential with Empress?

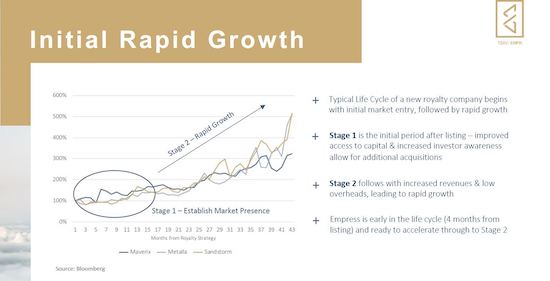

Here’s another chart that will give you an idea.

|

| |

| Click image for more detail

|

The chart measures the share price performances of three advanced-stage royalty companies when they were at Empress Royalty’s stage of development.

|

As you can see, after a period of acquisitions spurred by access to capital, these companies made the pivot to revenue generation…and saw their valuations soar as much at 500%.

|

Thanks to its uncommon access to capital via its partnerships with Endeavour Financial, Terra Capital and Accendo Banco, Empress is moving through this initial development stage at lightning speed.

With the lucrative pivot to revenues and cash flow happening as we speak (and with a full pipeline of potential deals under review), Empress Royalty is trading at levels that make it a smart-money bet on the royalty and streaming sector.

But you don’t want to wait too long to consider investing in Empress — if gold prices start to take off, the bargain entry point offered by current trading levels could disappear in a flash.

|

|

.png)