|

Tres Cruces is a gold project in Peru that spent the better part of the last 17 years in hibernation.

|

That’s because major Barrick Gold had joint ventured the project back in the early 2000s and then taken its sweet time deciding whether to complete its earn-in on Tres Cruces.

|

In the end, the major decided not to complete the earn-in...and a massive, multi-million-ounce gold deposit fell back into the hands of the company that would become Anacortes Mining (XYZ.V; XYZFF.OTC).

|

That set Anacortes on a path to prove up the value at Tres Cruces, starting with a preliminary economic assessment of its near-surface oxide resource.

As you’re about to see, that report, released just last week, shows a profitable mining operation worth a multiple of Anacortes’ current market cap.

And here’s the best part: That near-surface resource is just the tip of the iceberg in terms of Tres Cruces’ potential.

The fact is, a much larger sulphide gold resource lies below the oxide resource and, with historic drill holes having ended in rich gold mineralization, the resource is set to grow with further drilling.

It all adds up to one of the more compelling gold opportunities of 2022, one you’ll want to consider before the drills finally start turning again at Tres Cruces.

|

A Near-Surface Gold Resource

Practically Begging To Be Mined

|

Last week’s PEA showed Tres Cruces’ oxide resource to have impressive economics using a heap leach operation.

At $1,700 gold, the after-tax net present value (NPV), discounted at 5%, is US$165.9 million — more than three times Anacortes’ current market cap. The internal rate of return (IRR) is a hefty 33%.

|

| |

| An impressive preliminary economic assessment: The oxide portion of the resource at Tres Cruces has an after-tax net present value of $165.9 million and is projected to generate a rich rate of return (IRR) of 33.0%.

|

The mine has an initial capital expense of just $125.2 million to build and would support an operation that would produce 68,000 ounces of gold per year over a seven-year mine life.

Better still, that resource valuation was based on a conservative gold price of $1,700/oz. At $2040 gold, the after-tax NPV jumps to US$240.7 million, and the IRR jumps to an exceptionally rich 42.6%.

|

Just Scratching The Surface:

A Much Larger Sulphide Resource Lies Below

|

Anacortes’ plan is simple and powerful: Put this mid-sized but exceedingly profitable resource into production while it looks at developing the large sulphide resource that lies below the oxide pit at Tres Cruces.

|

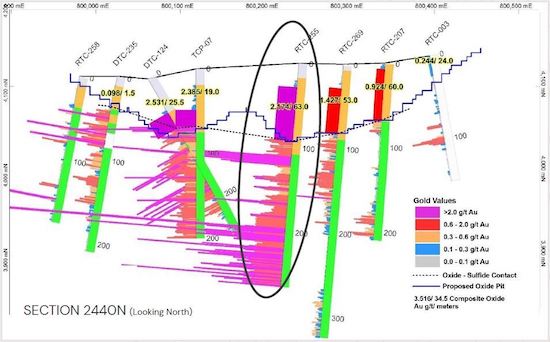

That sulphide resource currently stands at 1.8 million ounces...and remains wide open at depth. Anacortes plans to drill this resource off, following up on key holes drilled when the Barrick JV was still in effect.

|

Those holes include 228 meters of 2.95 g/t gold in hole RTC-255. Notably, that hole ended in mineralization.

|

| |

| Hole RTC255 at Tres Cruces hit a long, 295-meter interval of 2.95 g/t gold that went far below the projected pit outline for its near-surface oxide resource.

|

That’s an intersection that would have sent the prior company’s share price soaring, but because it came out in conjunction with Barrick’s sporadic work on the project, that great hit got lost in the shuffle.

Now, Anacortes plans to drill at depth at Tres Cruces, and that program will include a near-twinning of holes like this.

|

Thus, odds are excellent that Anacortes will serve up a very impressive set of assays in the coming months.

|

And with the valuation of Tres Cruces already backstopped by the oxide resource, you’ll get all this exploration upside essentially for free.

Save

Not A Subscriber Yet?

Get Golden Opportunities For Free

Subscribe to our Golden Opportunities e-letter to receive timely market

updates from the Gold Newsletter research team, plus video

presentations by expert speakers from the New Orleans Conference

— and the Investor’s Guide to Gold and Silver — all at no cost!

CLICK HERE to start your subscription.

|

|

The risk-reward setup for Anacortes is firmly in our favor. The established value of a high-grade oxide gold resource...one that’s worth a multiple of the company’s market cap...makes the company a compelling lever on rising gold prices.

But the highly prospective exploration potential — the likelihood of adding to a multi-million-ounce oxide and sulphide resource via the drill bit in the weeks just ahead — will provide another potential path toward a significant price re-rating.

If you’ve been watching gold’s action of late, you know we’re in bull market territory. Russia’s war with Ukraine is driving the prices of commodities like oil and gold through the roof.

More to the point, gold is the only money that isn’t some government’s liability. As such, it’s the natural hedge against inflation.

|

In short, in an environment that’s made for gold, Anacortes Mining is a company made to leverage the yellow metal.

|

Current trading levels make Anacortes a name you’ll want to look at closely as gold extends its bull run.

|

.png)