| Editor’s Note: We’re happy to present another insightful contribution from our friend Danielle DiMartino Booth.

Danielle is widely recognized as today’s top expert on Federal Reserve operations and policy moves, and she will be presenting her latest views and forecasts next month at this year’s New Orleans Investment Conference.

She will join dozens of today’s top experts at this event, and we urge you to not only explore her valuable subscription services (see more by clicking on the link at the end of this article), but also to learn more about the exciting roster of speakers at the New Orleans Conference by clicking here.

— Brien

|

| Make Labor Day Great Again

|

| “It is not the employer who pays the wages. Employers only handle the money. It is the customer who pays the wages.”

- Henry Ford

|

| By Danielle DiMartino-Booth

Quill Intelligence

|

| The good news was productivity was roaring. What had taken 12.5 hours to build now took 93 minutes. The bad news: Workers wanted no part of this miracle. The year was 1913. Turnover at Ford Motor Corporation was rife. At 370%, each assembly line position saw more than three individuals cycle through in a calendar year. Such was the mind-numbing and physically grueling nature of rote.

To Henry Ford, the solution was simple. And so, he doubled his employees pay to $5 a day while cutting their workday to eight hours from nine. To his benefit, the two-shift capacity became three. Within a year, turnover had collapsed to 16%. Throughput, meanwhile, jumped by 40%. In 1919, as the Roaring Twenties beckoned, a Model T that had once fetched an $800 price now cost only $350.

To Henry Ford’s way of thinking, “We believe in making 20,000 employees prosperous and contented rather than just making a few of our executives millionaires."

George Pullman did not share Ford’s philosophy: “You give workers only as much as they basically need to survive. Thriving is something that management should do and that workers don’t have a right to do.” Following the depression of 1893, Pullman cut already low workers’ wages by 25% but did not reduce rents in its company town near Chicago. Starvation threatened many a family. The strike that followed the following summer was “resolved” when federal troops intervened, killing 30 men and wounding 57. As a conciliatory gesture, President Grover Cleveland designated Labor Day a federal holiday.

Today, CEOs make 350 times more than their employees; the ratio has risen from 20:1 in 1950. The Democratic Party that once represented the economy’s workers bees is now equally beholden to Corporate America’s lobbying dollars. Public education is flirting with being predominantly centered in enclaves of the privileged few whose street addresses end with the right zip codes. The backdrop was ripe for a shot at socialism, which progressives took for a spin. The upshot: The worst policy error in a generation landed inflation at a 40-year high.

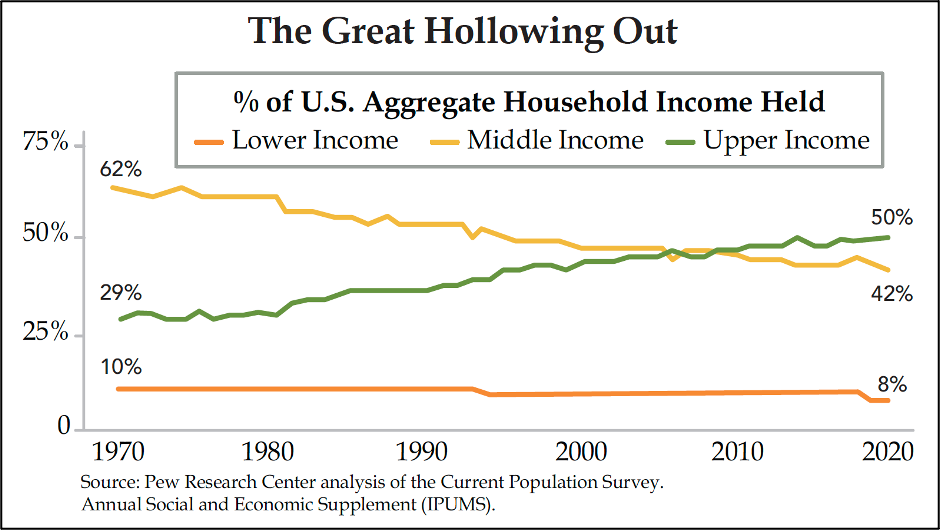

This isn’t the first time I’ve shared this graph, nor will it be the last. In the years since I was born, U.S. middle income earners have been whittled down from the majority to a shrinking faction. Lower-income earners have barely benefitted while the fruits of inequality have advanced the growing share of upper-income earners.

|

| There is good news here. Incomes sufficient to qualify for the top tercile indicate a better way of life spread across a widened swath of the population. But ask of the strength of a nation’s foundation as its middle is hollowed out? What will become of those at the top if a tough talking Federal Reserve Chair Jerome Powell and his apparent acolytes on the Federal Open Market Committee follow through with their threats to normalize monetary policy?

While I openly applaud the spirit of destroying the Fed Put, the risks cannot be glossed over as a matter of principle. In the same manner there is no way to steer an economic recovery built on increasing indebtedness to a soft landing, there is no way the societal fabric of America will not unravel if the Fed succeeds. The time has come to contemplate an existential manifestation of systemic risk.

After reading today’s abbreviated Weekly Quill, I would ask that you join me in envisioning the dangerous place in which the United States finds itself historically.

It is naïve to shrug off where this country has found itself believing that handing matters over to others will never personally affect us. Indeed, the “dry” financial subjects of auto repossessions and evictions illustrate societal systemic risk. Google “eviction murder.” You will find five news stories from Alaska, Arizona, Ohio, Oklahoma and Texas. A total of 11 lay dead in the wake of the last week’s carnage. Switch out “eviction” for “repossession” and you’ll find yourself reading similarly horrific headlines. And this is with an unemployment rate at a half-century low, one that’s poised to rise in what will be a shock to an anesthetized system.

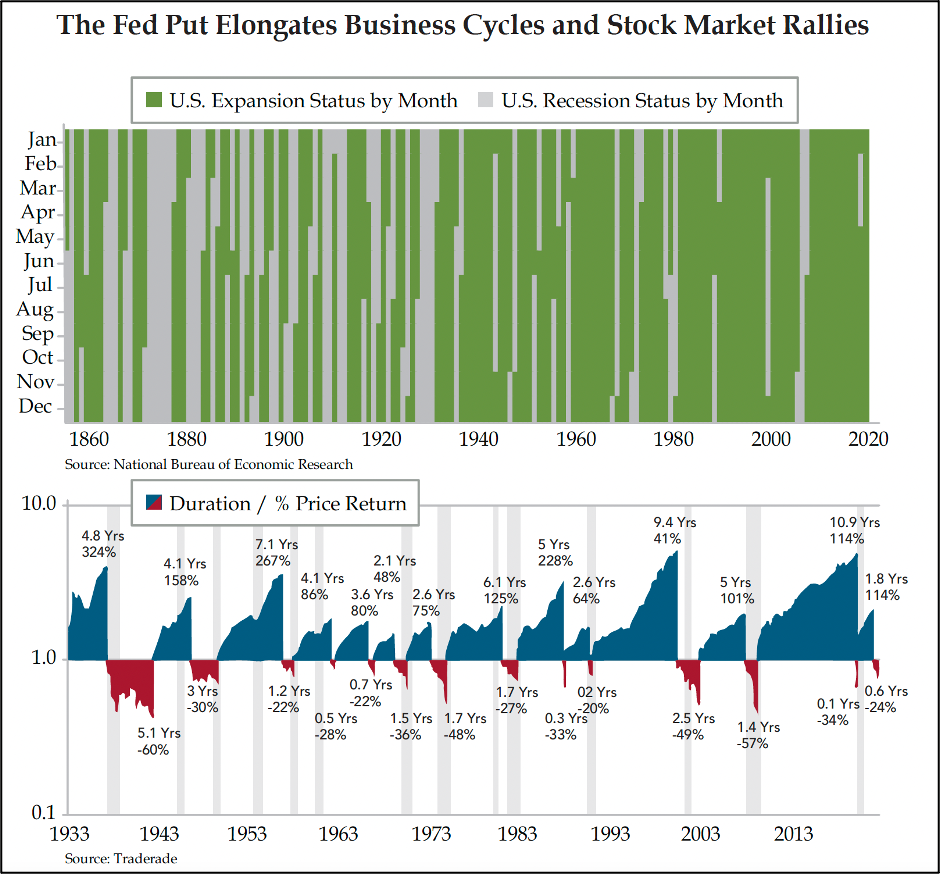

All economies that evolve from emerging to developed status enjoy increasingly long periods of recovery vis-à-vis recession. The process can, however, be reversed. The birth of the Fed Put began 35 years ago this month, when Alan Greenspan succeeded Paul Volcker. Arresting the business cycle and sustaining elevated risky asset prices became the effective modus operandi. Price discovery and capitalism have since slowly bled out. Corruption and income inequality have taken their place threatening to sentence America to third world status.

I hate to recognize these realities. But I lived in Venezuela the summer before Hugo Chavez rose to power. My eyes don’t lie. The parallels are too multiple to deny.

|

| There are solutions. Term limits must be imposed and lobbying exorcized, freeing elected officials to reform public education, break up monopolies and appoint independent actors at federal

agencies. The Federal Reserve must be reformed, its independence restored allowing monetary policy to jettison the failures of zero interest rates and quantitative easing that enflame moral hazard. The power to undertake radical change rests with the United States’ reserve currency status; her sovereign debt is still the world’s risk-free asset. Diabolical despots rule its enemies, a strategic sovereign advantage.

Most importantly, good will remains in the hearts of most who still embrace the ideals of America’s founding fathers; to this silent majority who yearns for the middle class to rise anew, greed is not good, attaining the American Dream is. The leadership vacuums at the Federal Reserve, in Congress, and the White House must be filled by a fresh generation of those with the fortitude to wrench back the liberty for which U.S. soldiers have made the ultimate sacrifice.

|

.png)