| Is this today’s most undervalued exploration company?

| | | Please find below a special message from our advertising sponsor, ATAC Resources Ltd. Golden Opportunities is a free service that gives you valuable investment intelligence all year long at no charge, and advertisements allow us to continue sending these reports.

| |

The bear market in gold has created some extraordinary bargains, if you know where to look. One of the best right now seems to be ATAC Resources Ltd. (ATC.V; ATADF.OTCQB).

With millions of ounces of gold resources and C$4 million in cash providing a sturdy valuation backstop, ATAC is a smart-money bet on established gold in the ground and multiple, promising copper-gold projects.

| | | |

Limited downside. Huge upside.

|

That, in a nutshell, is the investment case for ATAC Resources Ltd. (ATC.V; ATADF.OTCQB), a Western Canada-based explorer with two gold deposits to its credit.

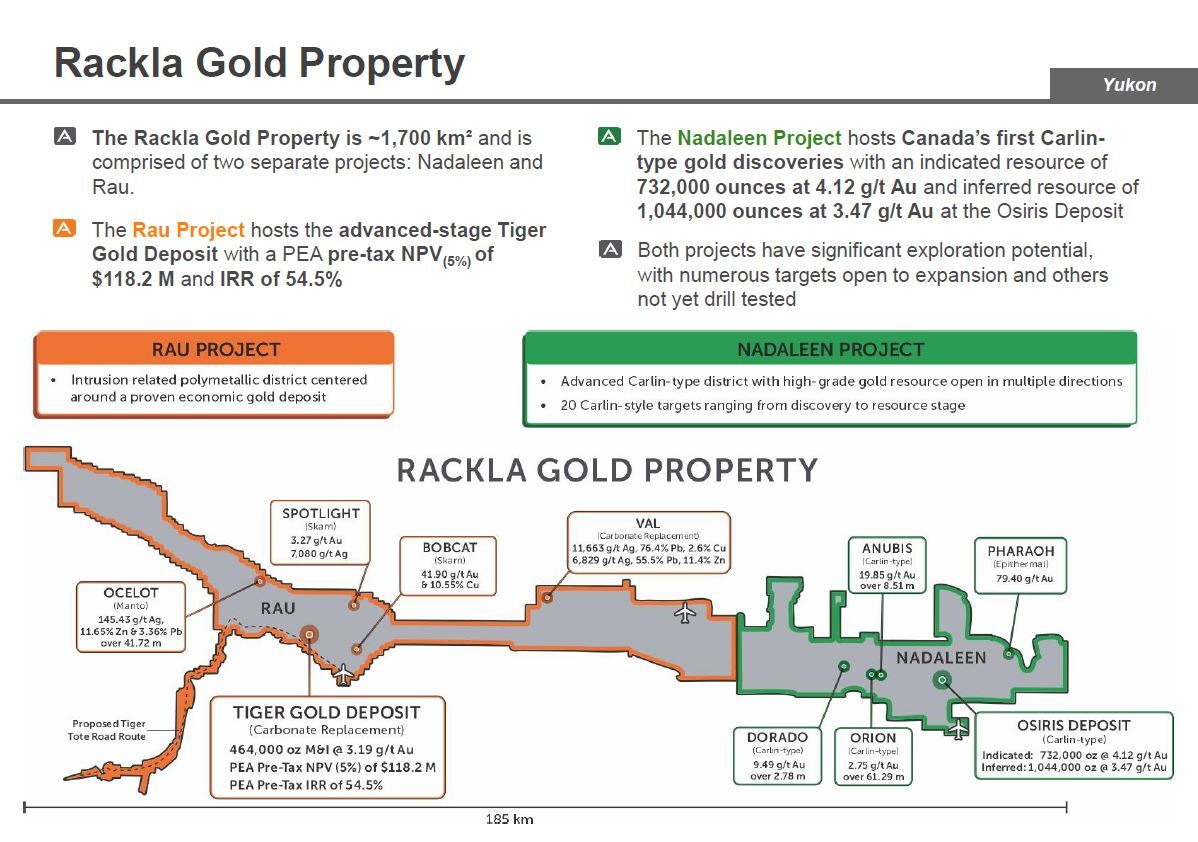

Those two gold deposits are located within ATAC’s district-scale Rackla property in the Yukon, and they are very large indeed.

|

The total resource includes 464,000 ounces of gold in the measured and indicated categories at one deposit...plus 732,000 ounces of indicated gold resource and 1.04 million ounces of inferred gold in the other. All at over 3 g/t gold.

|

One is at a PEA level. The other is part of a camp-scale land package that boasts no less than 17 other targets at a pre-resource stage.

On top of all this, the company controls a handful of copper-gold focused projects in the Yukon and British Columbia at earlier stages of development, plus C$4 million in cash.

The best news: The bear market in gold has put ATAC on sale.

|

Consider this: A company with all this going boasts just a C$16 million market cap.

|

Is there any wonder why ATAC could be considered the best bargain in today’s gold market? However, as you’re about to see, that low valuation could get re-rated dramatically upward soon.

|

Rau Provides Valuation Backstop

|

All by itself, the Tiger gold deposit on the Rackla property’s Rau project provides a sturdy valuation backstop to ATAC’s share price.

|

A preliminary economic assessment (PEA) completed on Tiger shows a pre-tax net present value, discounted at 5%, of C$118.2 million and an internal rate of return (IRR) of 54.5%. This study used US$1,400 gold, well below today’s price.

|

The deposit is open pittable and anchors the Rau property where numerous intrusion-related, polymetallic targets have been identified.

| | | | Click image to enlarge

|

The development prospects for Tiger and its sister Osiris deposit on the adjacent Nadaleen project have improved with the recent discovery of gold by other operators just to the southeast of the Nadaleen project.

ATAC’s management sees the entire district getting developed based on the combined potential of this burgeoning area.

Save

Not A Subscriber Yet?

Get Golden Opportunities For Free

Subscribe to our Golden Opportunities e-letter to receive timely market

updates from the Gold Newsletter research team, plus video

presentations by expert speakers from the New Orleans Conference

— and the Investor’s Guide to Gold and Silver — all at no cost!

CLICK HERE to start your subscription.

|

Nadaleen Hosts Carlin-Style Gold Mineralization

|

Their hopes for the region are underpinned by the second deposit ATAC has outlined at Nadaleen.

|

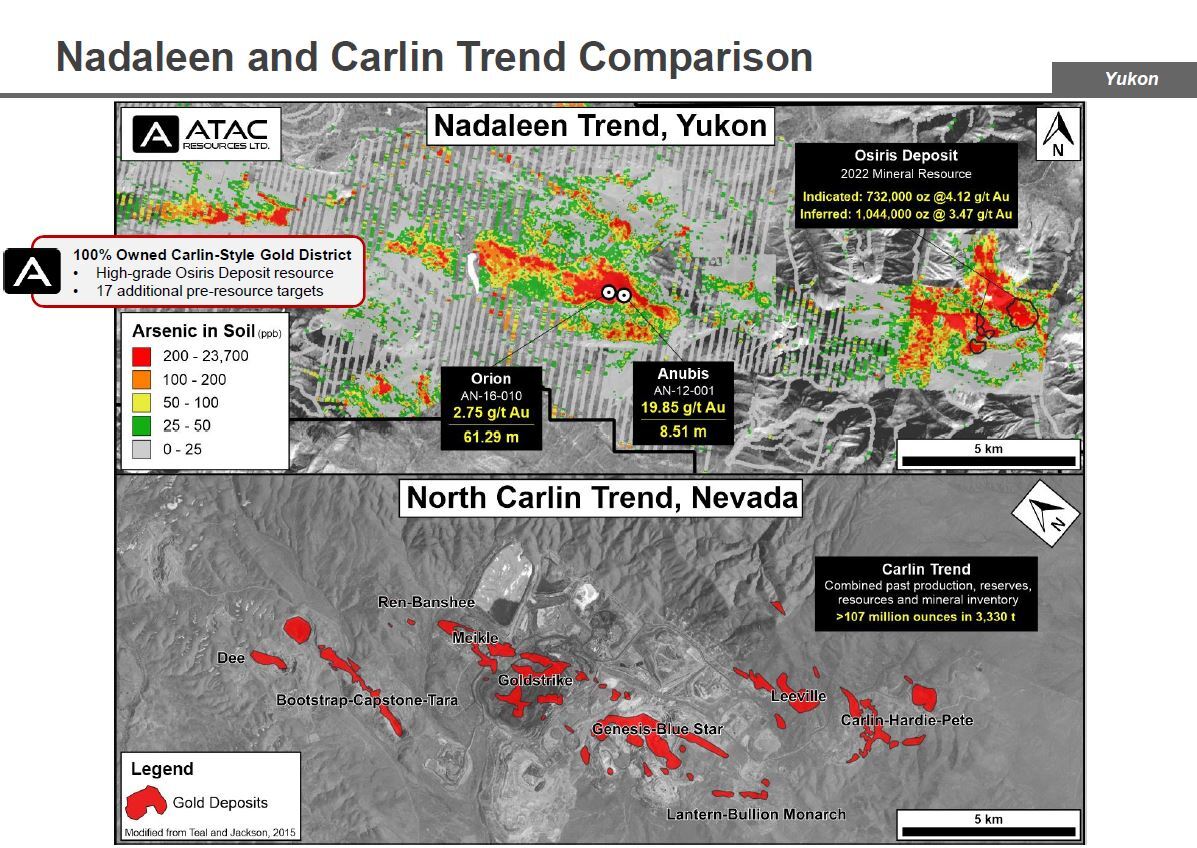

What makes Nadaleen unique is that it’s home to open-pittable, Carlin-style gold. It’s one of the very rare instances that this deposit type has been discovered outside of Nevada.

|

Why is that important? The map below explains why.

| | | | Click image to enlarge

|

As you can see, the scale of the Nadaleen project compares favorably with the Carlin Trend in Nevada — which features fully 107 million ounces of gold in resource inventory.

Nadaleen is obviously at a much earlier stage and its ultimate potential is still unknown.

But the combination of what is already proven and the blue-sky upside is impressive: Between the Osiris deposit (732,000 ounces indicated gold and 1.04 million ounces inferred gold) and the 17 pre-resource targets outlined at Nadaleen, the project has the scale to host another Carlin district, thousands of miles to the north.

|

Plus:

An Array Of Early-Stage Copper Projects

|

In addition to the exceptional value and exploration upside of Rackla, ATAC has amassed a remarkable collection of highly prospective copper projects in the Yukon and British Columbia.

Those include:

|

• The PIL property: This large, under-explored land package lies in the heart of British Columbia’s Toodoggone district amongst multiple past producing mines and advanced exploration projects. 2022 prospecting at PIL returned samples as high as 18.4% copper and 78.3 g/t gold.

• The Catch property: This western Yukon project is a new copper-gold discovery where geochemical work has identified a 5,000-meter-by-500-meter copper-gold-in-soil anomaly. The best rock samples from Catch include 52.4 g/t gold, 1.60% copper and 41.7 g/t silver.

• The Connaught property: Located 65 kilometers west of Dawson City, Yukon, ATAC’s Connaught project has seen no historic exploration for its porphyry potential. Assay are pending from an RC drilling program to test for large, copper-gold-hosting porphyries.

| |

And considering the value already established at Rackla, an investor at current prices gets all this copper-gold upside essentially for free.

|

Huge Upside, Minimal Downside

|

Think about ATAC Resources’ approximate C$16 million market cap for a moment.

For a share price of around just C$0.075, you get a company that boasts the following:

|

• A PEA-level project that all by itself is worth several multiples of ATAC’s current market cap...

• A large and high-grade gold resource at Nadaleen that’s an analog for the prolific Carlin gold trend in Nevada...

• An attractive package of copper-gold exploration projects on top of it all, essentially for free at the company’s current market value...

• And $4 million cash position to move this impressive project portfolio forward.

|

In the current market, that cash position is a true advantage, as most juniors are having trouble raising money at any price.

|

Bottom line: ATAC Resources may be today’s most under-valued junior mining company.

|

This market anomaly is a result of not only the bear market in gold, but also the fact that ATAC’s management — one of the most respected in the business — has worked tirelessly to build value without tooting its own horn.

That situation is changing at this moment, as the management team is determined to get ATAC’s story out. And the timing is perfect as, with the metals now perking up, the company’s share price could get a dramatic re-rating as investors discover this extraordinary situation.

Things are moving quickly, and the time to dig into ATAC’s remarkable value proposition is now.

|

CLICK HERE

To Learn More about ATAC Resources Ltd.

| | | |

© Golden Opportunities, 2009 - 2022

| | Advertisements included in this issue do not constitute endorsements from us of any stock or investment recommendation made by our advertisers.

Warnings and Disclaimers: As you know, every investment entails risk. Golden Opportunities hasn’t researched and cannot assess the suitability of any investments mentioned or advertised by our advertisers. We recommend you conduct your own due diligence and consult with your financial adviser before entering into any type of financial investment. This profile should be viewed as a paid advertisement. The publisher and staff

of this publication may hold positions in the securities of companies discussed or recommended. The information contained herein has been received from sources which the publisher deems reliable. However, the publisher cannot guarantee that such information is complete and true in all respects. The advertiser provided a review of the factual content of this advertisement at the time of publication. The publisher

is not a registered investment adviser and does not purport to offer personalized investment related advice; the publisher does not determine the suitability of advice and recommendations contained herein for any reader. Each person must separately determine whether such advice and recommendations are suitable and whether they fit within such person’s goals and portfolio. The advertiser featured in this edition of Golden

Opportunities has paid the publisher for the costs and compensation related to the authorship, overhead, design and distributing this online edition, in the amount of $7,500. The publisher may receive revenue, the amount of which cannot be predetermined, from sales resulting from any accompanying offer. Authors of articles contained herein may have been compensated for their services in preparing such articles.

Golden Opportunities

Jefferson Companies

111 Veterans Memorial Blvd. Suite 1555

New Orleans, LA 70005

1-800-648-8411

| | | |

.png)