|

| In a world hungry for new, open-pittable gold mines, $3,300/oz. gold is minting a new class of wildly profitable deposits.

|

| One of today’s most compelling examples is Vista Gold’s (VGZ.TO; VGZ.NYSE-A) Mt Todd project in Australia’s Northern Territory.

|

| A 2024 feasibility study on Mt Todd had envisioned a massive, 50,000 tonne-per-day operation with a tough-to-finance $1.03 billion initial capital expense to build it.

But with gold trading at sky-high levels, Vista’s management team saw the potential to trade scale for “financeability.”

The result?

A new feasibility study for a 15,000-tpd, fit-for-purpose gold mine at Mt Todd that envisions a still-large, 30-year operation...but with a dramatically lower initial capex and an even higher average gold grade.

|

| As you’re about to discover, the new feasibility study is a paradigm shift for Mt Todd, one that will now hand Vista Gold an array of options for advancing the project.

|

| Simply put, the new plan provides a clearer path to turn record-high gold prices into rich profits.

But the market has yet to wake up to this new potential, making this the perfect time to learn more about Vista Gold.

|

| A Paradigm Shift

|

| With the new fit-for-purpose design for Mt Todd, Vista has produced a model for development that prioritizes grade over tonnes.

|

| Yet Mt Todd is so large that even this reduced plan results in a world-class project: The mine is now slated to generate a remarkable 153,000 ounces of gold per year in the first 15 years of a 30-year mine life.

|

| It will use contract mining and power generation, along with a “fly-in, fly-out” workforce that will result in a significant 59% reduction in initial capital expense.

Following this model puts Mt Todd in the company of many highly valued Australian peers. In fact, Vista is employing Australian consultants and engineers who have deep experience bringing similarly sized projects into production.

|

| Compelling Economics...

|

| And, as the slide below makes clear, right-sizing Mt Todd by no means diminishes its profitability...or the powerful leverage it offers on higher gold prices.

|

| |

| Click image to enlarge

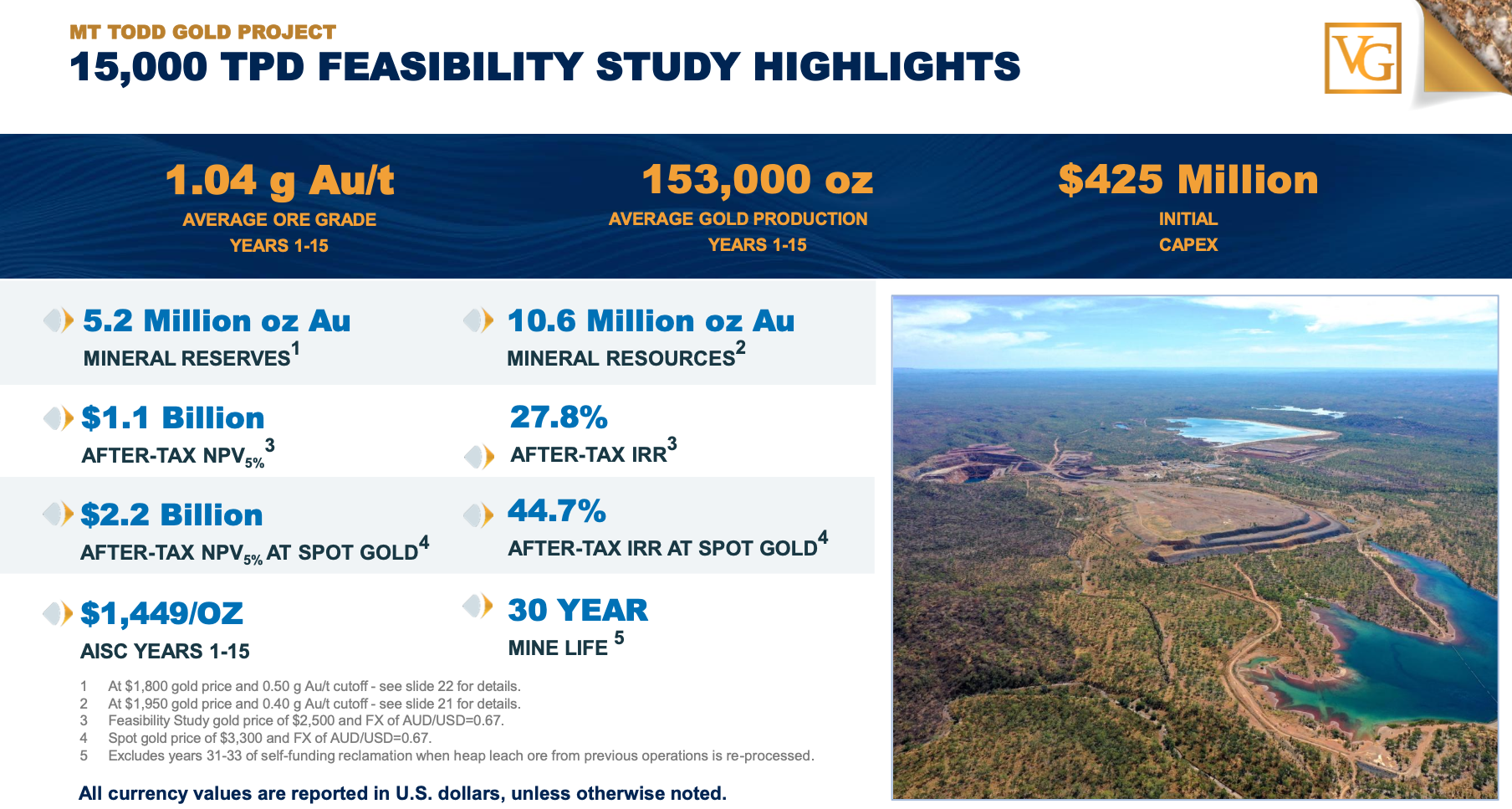

Even at a base-case gold price of just $2,500/oz., Mt Todd’s new, fit-for-purpose production model has an eye-popping $1.1 billion after-tax net present value.

|

| The new feasibility study envisions a mine that generates an average ore head grade of 1.04 g/t in the mine’s first 15 years — a grade equal to or greater than the average grade for open-pit gold mines across the globe.

More importantly, the economics still pop for Mt Todd. Even at the base-case price of $2,500/oz. gold, Vista projects an after-tax net present value, discounted at 5%, of $1.1 billion and a lucrative after-tax IRR of 27.8%.

|

| And consider this: At near-current spot prices of $3,300/oz., that after-tax NPV doubles to $2.2 billion and the after-tax IRR jumps to 44.7%.

|

| The new study envisions an initial capex of just $425 million, a number that should give Vista Gold a number of financing pathways to put Mt Todd into production.

|

| Options For Partnership, M&A And More...

|

| Those options include attracting a joint-venture partner or simply developing Mt Todd itself.

The new model’s dramatic reduction in initial capex and the project’s location in mining-friendly Australia should substantially increase the number of potential partners for the project.

Both mid-tier and major producers alike need mines that can significantly move the needle for their production profiles.

|

| The new plan for Mt Todd posits a mine that can certainly do that and, thanks to an extraordinary 10-million-ounce gold resource, it has options to scale up from here.

|

| Even if Vista elects to move the project forward on its own, it should be able to find willing financing sources to fund the development of this open pit mine.

And Mt Todd’s status as a brownfield project means that it has a lot of in-place infrastructure that can smooth the development process.

|

| Tremendously Undervalued...For Now

|

| Mt Todd’s base-case NPV under the new, fit-for-purpose model, is $1.1 billion...its value at current gold prices is $2.2 billion...and yet its current market cap is only around $120 million.

|

| |

| Click image to enlarge

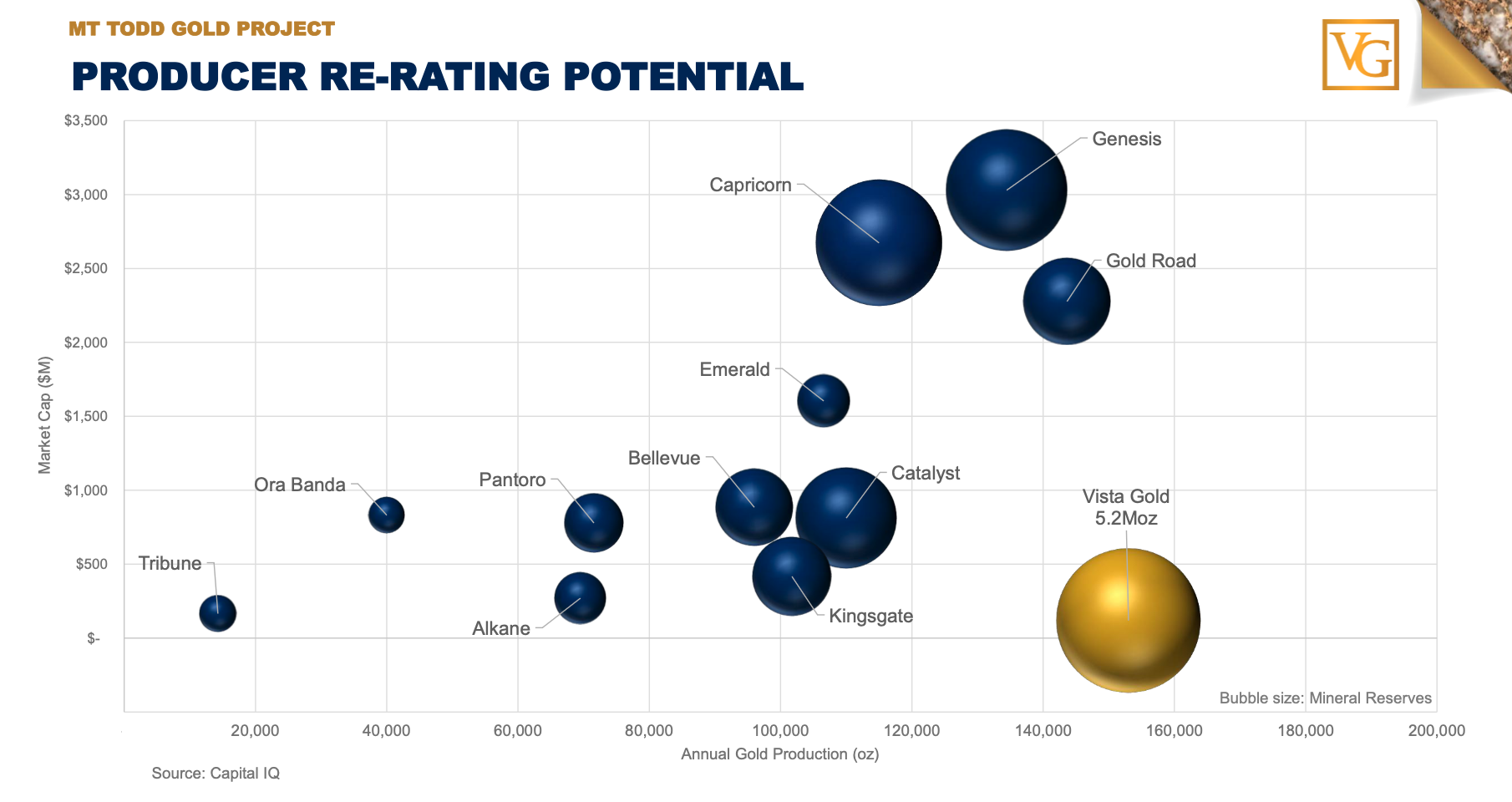

Vista Gold’s current market cap (indicated in gold above) is still just a fraction of other producers with comparably sized resources.

|

| The graph above plots the market values of various producers and potential producers against the average ounce-per-year production for their mines.

As you can see, Vista Gold and its 5.2 million ounces of gold reserves at Mt Todd stands out as perhaps the top re-rating opportunity in the entire gold market.

|

| Other producers with comparably sized mines are garnering as much as $2.5 billion-$3.0 billion market caps.

|

| Even if Vista Gold moves toward the base-case NPV for Mt Todd, a money-multiplying gain in the company’s share price could result.

Add in the prospect of $4,000/oz. gold in the next 12-18 months, and you have a gold story in Vista Gold that deserves your immediate attention.

|

| CLICK HERE

To Learn More about Vista Gold Corp.

|

.png)