| Is it time to sell?

| | You are receiving this message because you have specifically subscribed to Golden Opportunities, have purchased a product or have registered for a conference with us or with one of our partners. If you'd rather not receive emails from us, please click the link at the bottom of this page to unsubscribe from our database. Remember your personal information will never be rented or sold and you may unsubscribe at any time.

| | Contact Us | Privacy Policy | View in Browser | Forward to a Friend

| | | Are We There Yet?

| | A market update from one of today’s top resource-market and macroeconomic analysts.

| | Editor’s Note: Our friend Edward Bonner checks in today with another one of his, and his Sprott team’s, outstanding market analyses. Today Edward addresses the question that has sprung to many metals and mining investors’ minds after the furious rallies in gold and silver: “Should I sell?”

I hope you enjoy Edward’s contribution below. And feel free to contact him with any comments or questions via his contact information at the end of the article.

— BL

| | |

October 6, 2025

Dear Fellow Investor,

| | “The most talked about trade that nobody owns.”

– Ed Coyne, VP Sales, Sprott Asset Management

| | Is it time to sell?

Over the past few weeks, I have received multiple inbounds asking what to do about our precious metals exposure. As of the start of Q3, gold (XAU) is up over 45% while gold miners (GDX) are up over 100%. Most charts bare the resemblance of a hockey stick. Understandably, some of you might be getting a little nervous.

So, here’s my take.

On a purely technical basis, it is true that we are in overbought conditions, meaning the Relative Strength Index (RSI) – a measure of the speed and magnitude of a security’s recent price changes – is above its upper threshold. These moves are usually followed by a reversal to more neutral RSI levels, often accompanied by a pullback.

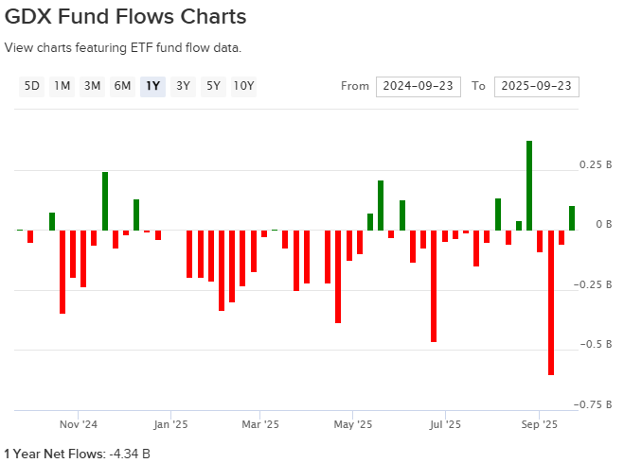

There are bound to be bumps along the way, especially after such a breathtaking climb, but I believe gold and particularly its miners remain remarkably under-owned. In fact, GDX fund flows are still net negative, having shed roughly 20% of its shares outstanding since the start of the year, as shown in the graph below.

| | | | While the longer-term setup for gold and its miners still looks attractive, I have to be pragmatic and seek to manage risk. With gold at inflation-adjusted all-time highs, for me, prudence is harvesting some profits, rebalancing my portfolio and building up cash reserves for a rainy day.

Risks of a near-term pullback may have increased ever so slightly with the flurry of ‘positive’ macro data received late last week (PMIs, GDP, jobless claims, new home sales, etc.), as it raises doubts over the need for further Fed rate cuts.

But make no mistake, I strongly believe we are still in an extremely accommodative environment where monetary and fiscal policy are working to suppress the dollar, lower real yields and increase overall liquidity.

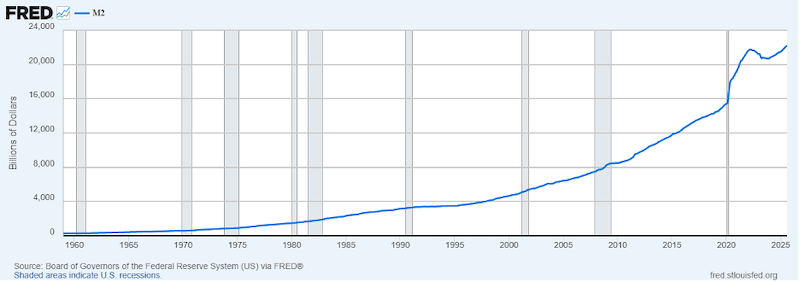

It’s no surprise that M2 money supply reached a new all-time high in August, as shown in the chart below from the Federal Reserve Bank of St Louis, dated 09/30/2025.

| | | | Year-over-year, M2 money supply increased by $1 Trillion. During that same period, the World Gold Council estimates that global gold mine production was approximately 135 million ounces. At today’s price of roughly $3,800/oz, that is about $500B, or about half of the increase in M2 money supply – or just under one fourth of new US federal debt added during the same period.

As of September 30th, 2025, US federal debt stood at a staggering $37.4 trillion…

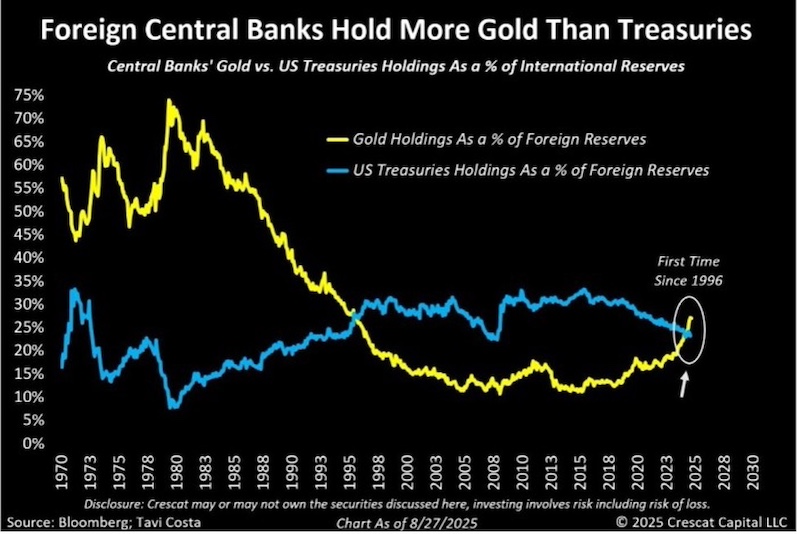

We aren’t the only ones who see a problem. As I’ve said before, I think the smart money has been making moves ever since the US chose to freeze Russia’s reserve assets. And now, for the first time since 1996, foreign central banks own more gold than US Treasuries.

|  | | It seems like gold has reclaimed its rightful place as the ultimate safe haven.

Jumping on the band wagon, major financial institutions are suddenly recommending gold as part of a diversified portfolio. In some instances, they even recommend replacing part of the bond allocation in a 60/40 portfolio to gold – the new 60/20/20 portfolio.

I must admit. That last part makes me nervous too… So, we go back to basics…

Beginning with some anecdotal evidence, my team and I were at the Beaver Creek Precious Metals Summit and the Denver Gold Show a few weeks ago. While attendees were obviously excited, we didn’t see signs of irrational exuberance and most of the people we saw were the same old faces we’ve seen a dozen times. No one new. Mining companies were talking about returning profits to shareholders, paying down debt, and remaining capital disciplined.

On a side note, at over 50% Free Cash Flow (FCF) margin, gold mining companies are looking like much better businesses than even the Mag 7. And most are still trading at or below 1x Net Asset Value (NAV).

These are not the signs of an over-crowded trade, in my opinion.

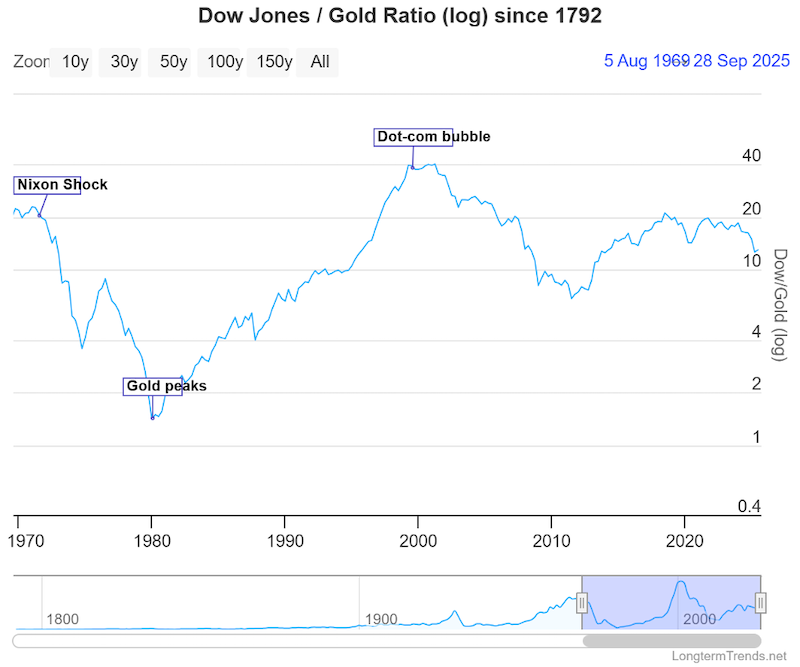

Looking at the ratio between the Dow Jones Industrial Average (DJIA) and gold, you can see that despite the recent rise, gold is still historically undervalued relative to the DJIA.

| | | | You can see the same relationship when looking at the entire commodities sector relative to the DJIA. For a long time now, commodities have been under-invested, leading to tighter and tighter mine supply. Arguably a positive setup for other raw materials with a finite supply and strong demand drivers (e.g. copper).

But I digress. The point is it looks like commodities are making a comeback, and gold is leading the charge. Yet still gold remains, “the most talked about trade that nobody owns.”

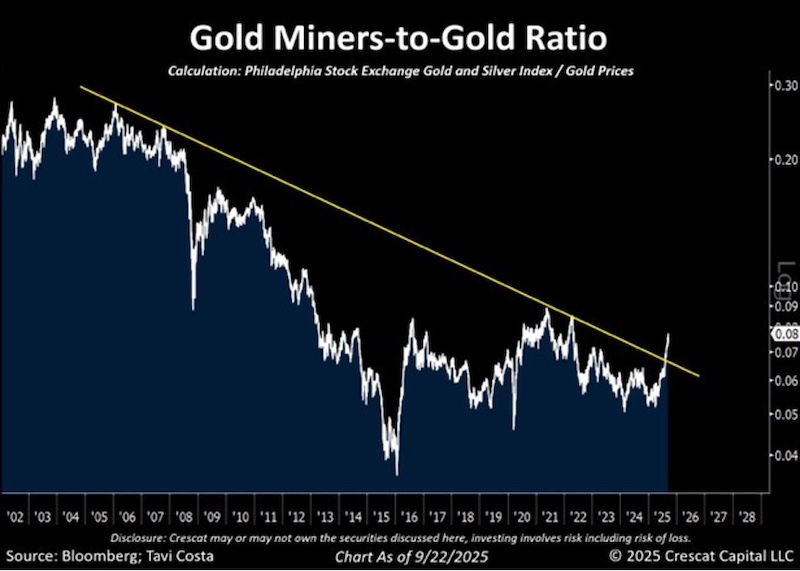

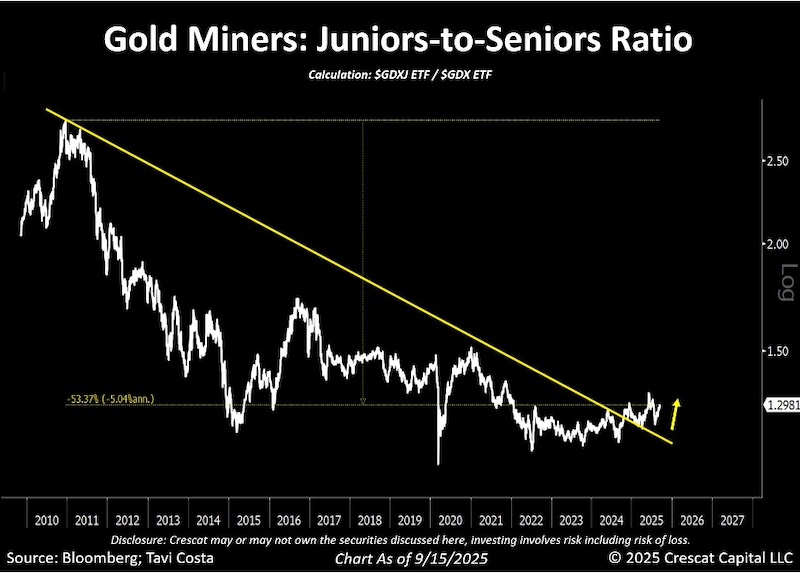

Finishing with two charts from Tavi Costa. If you don’t own gold mining equities, these charts might make you reconsider.

|  |  | | These both highlight how gold miners have long under-performed the physical metal but have just recently started to outperform. He goes on to point out how junior gold miners have broken out and are starting to outperform the more mature (and less leveraged) senior gold miners. Something to think about…

Hopefully this helped to address some of your concerns regarding the current bull market in precious metals. If you’re interested in working with an investment advisor to help manage your mining stock portfolio, please call or email and I’d be happy to help.

Best regards,

Edward

P.P.S. If you need help with managing your portfolio of mining equities, please reach out for a free consultation.

|  | | Edward Bonner

Investment Advisor, Geologist

ebonner@sprottglobal.com

Sprott Global Resource Investments Ltd.

1910 Palomar Point Way, #200

Carlsbad, CA 92008

| | Interested readers can contact me directly via email at ebonner@sprottglobal.com

| | Editor’s Note: Edward Bonner is an experienced exploration geologist and a graduate from the Colorado School of Mines with a Master’s in Economic Geology. He’s now helping many investors protect and build wealth as an investment advisor at Sprott Wealth Management.

| | Important Disclosure

Relative to other sectors, precious metals and natural resources investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Gold and precious metals are referred to with terms of art like store of value, safe haven and safe asset. These terms should not be construed to guarantee any form of investment safety. While “safe” assets like gold, Treasuries, money market funds and cash generally do not carry a high risk of loss relative to other asset classes, any asset may lose value, which may involve the complete loss of invested principal.

Past performance is no guarantee of future results. You cannot invest directly in an index. Investments, commentary, and opinions are unique and may not be reflective of any other Sprott entity or affiliate. Forward-looking language should not be construed as predictive. While third-party sources are believed to be reliable, Sprott makes no guarantee as to their accuracy or timeliness. This information does not constitute an offer or solicitation and may not be relied upon or considered to be the rendering of tax, legal, accounting or professional advice.

| | | | CLICK HERE to watch interviews by Brien Lundin and Kai Hoffmann with many of today's most exciting junior mining companies on the

Gold Newsletter Youtube channel.

| | | | © Golden Opportunities, 2009 - 2025

| | Advertisements included in this issue do not constitute endorsements from us of any stock or investment recommendation made by our advertisers.

As you know, every investment entails risk. Golden Opportunities hasn’t researched and cannot assess the suitability of any investments mentioned or advertised by our advertisers. We recommend you conduct your own due diligence and consult with your financial adviser before entering into any type of financial investment.

Golden Opportunities

Jefferson Companies

2117 Veterans Memorial Blvd., #185

Metairie, LA 70002

1-800-648-8411

| | | |

.png)