|

| The combination of a world-class address, an under-drilled resource with enormous room to grow and a team that already has boots on the ground doesn’t come together very often.

|

| When it does, you pay attention.

|

| That combination is exactly what Tincorp (TIN.V; TINFF.OTC) has assembled. And the story is just getting started.

|

| In late February, Tincorp announced a definitive agreement to acquire the Santa Barbara Gold-Copper project from Silvercorp Metals.

Why would Silvercorp part with it?

Simple. Silvercorp is building four mines sequentially around the globe. And Santa Barbara (a copper-gold porphyry system) isn’t naturally synergistic with Silvercorp’s flagship Condor project just 10 kilometers to the north, which is an epithermal gold deposit.

That different geology demands a different development pathway and different capital requirements.

For Tincorp...and for Silvercorp, which has a big stake in Tincorp...the deal is a perfect fit. And the timing couldn’t be better.

|

| The Belt That Breeds Giants

|

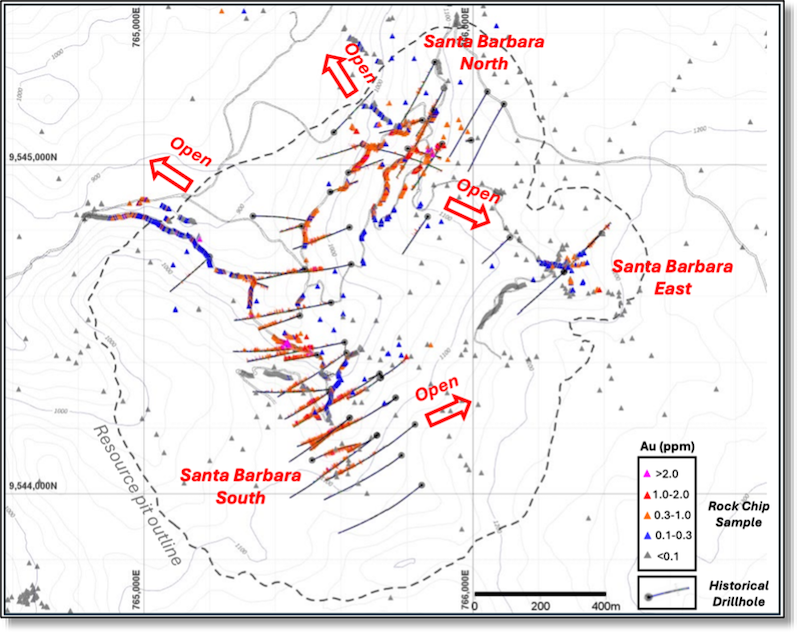

| Santa Barbara sits in the Zamora Copper-Gold Belt in southeastern Ecuador — one of the most prolific metallogenic belts in the Americas.

This is the neighborhood that holds Lundin Gold’s Fruta del Norte mine, CRCC-Tongguan’s Mirador copper-gold mine and Solaris Resources’ Warintza deposit. No less than three world-class assets within a 100-kilometer radius.

Santa Barbara is the only gold-dominant porphyry in that string.

And porphyries of this scale — coherent, continuous, open in all directions — don’t come available very often.

|

| An Already World-Class Resource

|

| Tincorp filed an updated resource estimate in early April using a gold price assumption of US$3,200 per ounce and a copper price of US$12,000 per tonne, far more reflective of today’s market than the US$1,500 per ounce gold price used in the 2021 estimate for Santa Barbara.

The result: 697,000 ounces of indicated gold at 0.73 g/t, plus another 3.42 million ounces of inferred gold at 0.52 g/t. Combined with 494 million pounds of copper across all categories, the total gold-equivalent resource sits at approximately 4.3 million ounces.

That’s a very big number for a company at Tincorp’s current market cap. And it looks likely to get much larger very soon:

|

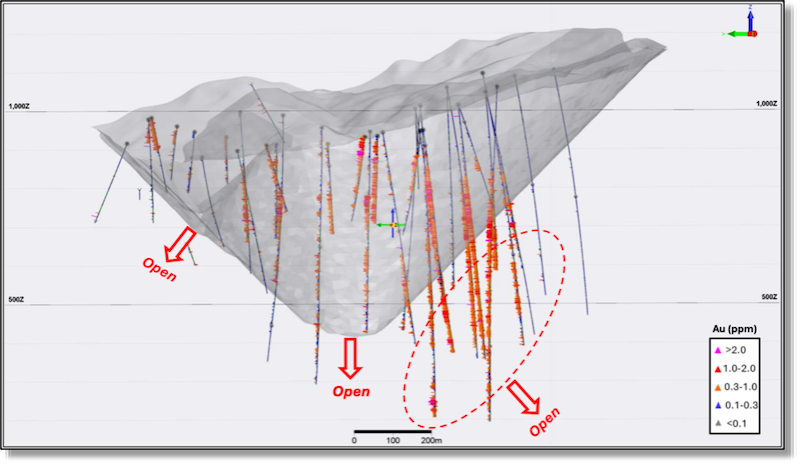

| Consider that only 56 drill holes over three decades of intermittent work — just 22,027 meters of drilling in total — has ever been done at this project.

|

| Despite no drilling at all since 2018, the deposit already measures 1.2 kilometers north to south, 600 meters east to west and extends more than 900 meters in depth.

And it remains open in every direction.

|

| Near Surface And High Grade

|

| At the northern end of the deposit, mineralization ideally comes right to surface. One section here runs 44 meters from surface at a remarkable 1.40 g/t gold.

|

| The shallow profile here suggests multiple high-grade starter pits that could dramatically improve project economics right out of the gate.

|

| The southern end tells a different story. Deeper, longer intervals with strong gold grades extending both within and below the current pit shell.

The deposit already has drill holes going well beyond the modeled pit.

|

|

| Past drilling has identified strong mineralization deeper than the current-planned pit shell, which should be accessible if Phase 2 drilling widens the pit as expected.

|

| When management talks about widening that pit to capture deeper mineralization, they’re not speculating.

The system is open at depth, to the east, northwest and at multiple untested targets identified through historical IP surveys and geochemical sampling. The company’s drill pograms will chase all of it.

|

|

| Santa Barbara is also open to expansion in multiple directions laterally, all of which will be targeted in Phase 2 drilling.

|

| Fully Funded And Moving Fast...

|

| In March, Tincorp closed a C$17.5 million subscription receipt offering, upsized from the original C$16 million target with full exercise of the overallotment option.

|

| The resulting share structure is still drum-tight: Insiders and associates participated heavily and will hold approximately 47% of the company post-closing.

|

| That number is significant. With Silvercorp retaining just under 28% of shares outstanding, roughly 75% of the stock is controlled by Silvercorp or insiders. The freely tradeable float sits at around 25%.

Shares will be hard to buy unless the price is right.

The financing covers drill programs, the first two payments to Silvercorp and general operating expenses. Management says the goal is 50,000 meters in the ground by end of Q1 2027.

|

| The initial focus of drilling will likely be to upgrade existing inferred resources to indicated, which should also push average grades higher in the process.

After that, drills will target expansion of the pit shell and step-out drilling on identified targets.

|

| In short, lots of drilling and news flow ahead.

And if the track record of this team is any guide, the news will come sooner and more frequently than the market may now expect.

|

| The Biggest Factor:

The Team Behind It

|

| The management story behind Tincorp revolves around Dr. Rui Feng.

|

| As the founder of leading global silver producer Silvercorp...as well as another spectacular success in New Pacific Metals...Feng’s unblemished track record is a key element in the Tincorp story.

|

| Moreover, his deep familiarity with the asset, the jurisdiction and the technical challenges ahead is not a minor detail.

Interim CEO Victor Feng is leading the acquisition on the ground, and technical director Alex Zhang round out a team with direct Ecuador experience.

That experience pays immediate dividends.

Also remember that Silvercorp was already operating in Ecuador before this deal.

|

| The institutional knowledge, in-country relationships and existing operational framework carry over to Tincorp.

|

| Most junior acquisitions come with a long runway of setup time before a drill ever turns. Not this one.

|

| The Opportunity Right Now...

|

| At its simplest, this is a re-rate story with very near-term catalysts.

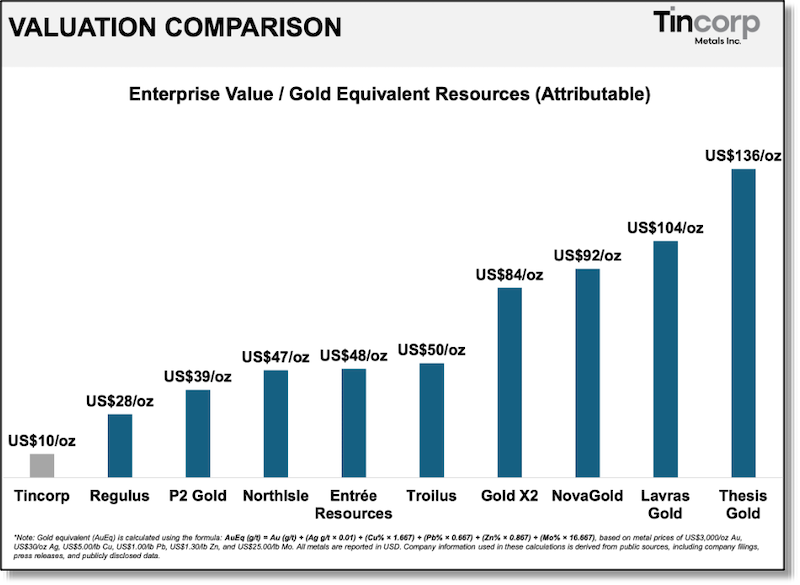

For one, Tincorp’s stock trades at a steep discount to peers on an EV-per-ounce basis.

|

|

| Tincorp is trading at a much lower resource valuation relative to its peers.

|

| And more: Insider ownership is substantial. The float is constrained. The resource is large, shallow in key areas and wide open for expansion.

For investors who prefer their upside with an exit optionality angle: Ecuador is seeing a wave of M&A activity, with major producers and well-capitalized acquirers increasingly active across the Zamora belt.

For a project of this scale in this address, that’s worth keeping in mind.

|

| The key here is that most junior resource companies hope to discover a multi-million-ounce deposit. Tincorp is starting with one.

|

| And it’s continuing to build that deposit as a well-funded, aggressive gold-copper developer anchored by a generational asset in one of the best mining belts in the world.

And the best part: The market hasn’t priced that in yet.

|

| CLICK HERE

To Learn More About Tincorp

|

.png)