|

| The junior mining market is famously inefficient. It often temporarily overlooks real values and extraordinary prospects.

|

| That frustrates some investors. But for the prepared, it’s not a bug. It’s a feature.

And sometimes it presents an extraordinary opportunity.

In today’s red-hot metals and mining market, Cassiar Gold (GLDC.V; CGLCF.OTC) looks like one of those extraordinary opportunities.

Consider these facts:

|

| Cassiar controls a massive, 590-square-kilometer land position in gold-rich northern British Columbia — a district-scale footprint with road access, grid power and permits.

This is no prospector’s dream. The company has so far outlined 1.9 million ounces of inferred gold resources, plus another 410,000 ounces of indicated resources.

And here’s the kicker: In a textbook example of the inefficient junior mining market, Cassiar’s 2.34 million ounces across all gold categories is still valued at just $18/ounce.

|

| And there’s more to come: With less than 0.3% of the land package having seen systematic exploration, the company has only scratched the surface of the potential ahead.

|

|

| Click image to enlarge

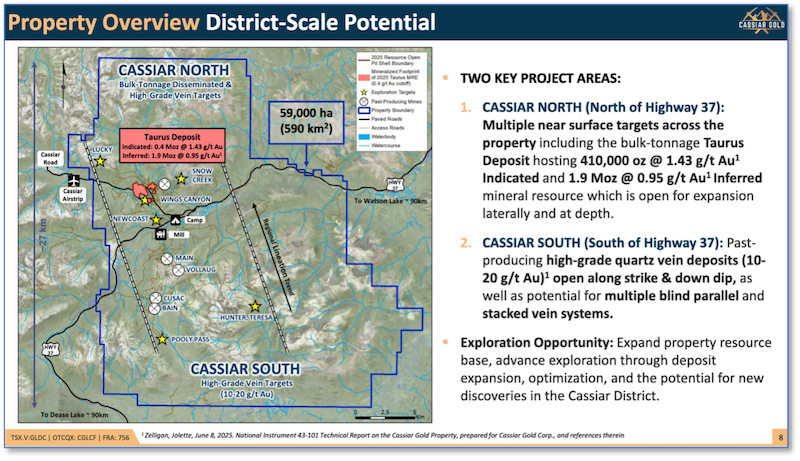

The Cassiar Gold property spans 590 square kilometers boasting two main project areas: Cassiar North (with 2.34 million ounces in indicated and inferred gold resources) and high-grade Cassiar South, plus numerous untested targets.

|

| Let’s take a look at why this mispricing exists...and why it doesn’t seem likely to last much longer.

|

| Seeing What Others Are Overlooking

|

| In junior mining, price often leads narrative — until reality reasserts itself. That lag is where disciplined investors win.

Cassiar sits precisely in that gap. While some other juniors may have doubled or tripled as metals prices have soared in this bull market, GLDC has seen only a relatively modest move off the lows so far.

The reason isn’t geology or jurisdiction or any negative factor. It’s simply that the tiny junior mining market has temporarily overlooked this remarkable prospect.

|

| But geology does not care about markets. A pit-constrained, near-surface resource with friendly geometry, strong access and growth vectors builds intrinsic value regardless of the day-to-day tape.

|

| When that value compounds quietly — then surfaces through resource expansion, a second discovery or economic studies — the re-rating tends to be swift. That’s the feature at work in this sector.

And it’s why opportunities like Cassiar are rarer, and more powerful, in a bull market: The crowd hunts heat, not value. You have the chance to do the opposite.

|

| A District Few Have Priced In...Yet

|

| Cassiar’s scale is the sleeper. The company controls an immense 59,000-hectare district with highway access bisecting the property.

|

|

| Click image to enlarge

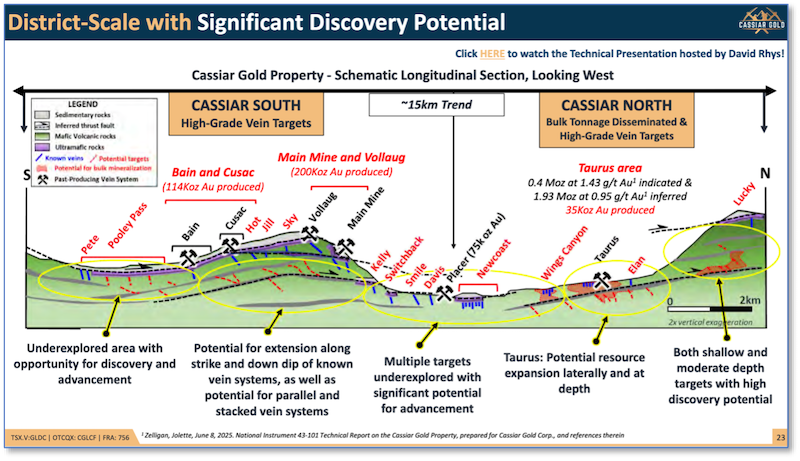

There’s remarkable value and massive untested potential on the Cassiar Gold property, with a string of untested and lightly tested gold targets lying between established gold resources.

|

| Despite that footprint, systematic work has touched only a tiny sliver of the land package. Management estimates that less than 0.3% has been explored to modern standards.

|

| That leaves a long list of untested or barely tested targets across both Cassiar North and Cassiar South — sheeted-vein bulk-tonnage analogs, high-grade orogenic veins, and structural repetitions that rhyme with known deposits.

|

| In short, the pipeline here is real. This is a district at the beginning of a multi-year discovery arc, not the end.

|

| Taurus:

A World-Class, Near-Surface Foundation

|

| The anchor is Taurus — a near-surface, pit-constrained system with scale and geometry that matter in a rising gold price environment.

|

| The updated NI 43-101 resource estimate (effective June 8, 2025; 0.4 g/t cutoff; $2,400/oz gold) outlines 410,000 ounces at rich average grade of 1.43 g/t (Indicated) and 1.93 million ounces at 0.95 g/t (Inferred), for 2.34 million ounces total.

|

| Importantly, 91% of these ounces sit within 150 meters of surface.

Recent step-outs along a 1.3-kilometer corridor continued to hit above cutoff grades and push the shell outward to the south, east and west.

For example, Hole 25TA-245 at Taurus East cut 13.4 meters of 13.53 g/t gold from just 28.2 meters downhole, including 0.8 meter of 210.71 g/t with a 0.4-meter sub-interval of 369.00 g/t.

|

| Those spikes are not one-offs. They align with visible-gold vein domains emerging across Taurus, nested within broader halos that make near-surface tonnage work. This is how early economics improve — ounces near surface, with streaks of high grade.

|

| When a foundation like this grows laterally while seeding higher-grade trends, the market’s eventual response is rarely subtle.

|

| Newcoast:

The Second Engine The Market Hasn’t Yet Priced

|

| Two kilometers south of Taurus, Newcoast stretches across 4 kilometers of gold-bearing quartz veins within a 15-kilometer trend of deposits and past producers.

|

| Early drilling in 2023–24 already delivered bulk-style thicknesses (141.4 meters of 0.89 g/t gold), but the target remains lightly drilled relative to its scale. That’s important in a district where stacked shear zones and repeated stratigraphy can host multiple Taurus-like panels.

|

| In 2025, Cassiar completed 7,308 meters of drilling over 20 holes, including the deepest hole ever drilled at Newcoast (about 720 meters for Hole 25NC-013). Assays are still pending, but visuals from 25NC-010 and 25NC-013 show dense sheeted veining and sulphides in altered mafic volcanics — the Taurus recipe.

If assays confirm what the rocks are showing, Newcoast could effectively place a second Taurus-style system on the map.

|

| It all adds up to a rare setup: a very large and growing near-surface resource plus a pipeline target that could double the thesis.

|

| With 5,243 meters of Newcoast drilling in the lab and results slated to be released through next month, the stage is set.

And a credible second engine is exactly the sort of development that flips “overlooked” into “re-rated.”

|

| People, Permits and Power

|

| Great projects need great management. Cassiar’s leadership has discovered, permitted, built, operated and sold multi-billion-dollar gold mines. That matters when projects transition from resource growth to studies and development.

|

| Insider ownership sits around 14%, aligning incentives with shareholders. On the register, 29% institutional support (including Delbrook, U.S. Global, Sprott, Ixios, Myrmikan, EMA, Commodity Discovery Fund and Terra Capital) helps to validate Cassiar’s value and potential.

|

| Jurisdiction and infrastructure are also big plusses: The Cassiar project lies in mining friendly British Columbia and features paved highway access, grid power, water, a fully owned and permitted mill, and two existing mine permits.

|

| Gold For $18 An Ounce?

|

| As of August 2025, Cassiar reported roughly C$8.7 million in cash and deposits. The market currently values the company around US$42 million.

|

| Against 2.34 million near-surface ounces, that’s roughly US$18 per in-situ ounce — an extraordinarily inexpensive valuation for a district-scale, road-accessed, permitted-infrastructure story in a Tier-1 jurisdiction.

|

| This is a bargain that seems destined to end soon. Because, while the metals are soaring and junior mining stocks are finally playing catch up...Cassiar is about to get the market’s attention.

|

| Catalysts Just Ahead

|

| Cassiar’s 2025 drill program is complete, with about 7,300 meters of expansion and discovery drilling across Taurus and Newcoast.

|

| Results will be released through February — and with visible-gold hits and broader mineralized envelopes already logged in drill core at Taurus, great assays will not be surprising.

|

| Metallurgical work and the first PEA have started, with results guided for Q1 and Q2 2026, respectively. Those studies can translate geological potential into economic reality — allowing analysts and the market to finally put pencil to paper and solidify the project’s market value.

Each of these milestones compounds the same thesis: a temporarily mispriced district with multiple ways to win.

|

| Why This Mispricing Won’t Last

|

| Right now, the market has essentially assigned Cassiar a placeholder valuation. It reflects neither the value of the multi-million-ounce resource...the scale of the land package...nor the emerging second engine at Newcoast.

|

| That’s the opportunity. The tape is hot, bargains are scarce — and yet this district sits at about $18/oz with 91% of ounces near surface and a flood of assays on deck.

|

| When a growing bulk-tonnage foundation meets a potential parallel system — in a jurisdiction with permits, power and a team that’s done it before — the re-rating is usually a question of “when,” not “if.”

And in efficient markets, you rarely get to buy that “when” cheaply.

The opportunity is Cassiar Gold...and the urgency to begin your due diligence on this company is real.

|

| CLICK HERE

To Learn More about Cassiar Gold

|

.png)