February 2, 2026

Dear Fellow Investor,

|

| Everything isn’t always as it seems.

|

| With that opening statement, you’ve no doubt expected a wild-eyed tale of nefarious forces behind the crash in gold and silver.

Well, I’m here to tell you that — while we’re unlikely to ever get the full story — the craziest conspiracy theories abounding on social media are far from true. And so are the dismissive explanations of a speculative bubble-burst by mainstream media.

The truth, as usual, lies somewhere in between.

|

| Painful But Not Surprising

|

| Readers of this letter as well as Gold Newsletter are aware that I, like many of my respected fellow metals-market watchers, have been recommending profit taking on this latest surge in the metals.

|

| As I’ve stressed in my writing and speeches, this was like nothing we’ve ever seen before.

|

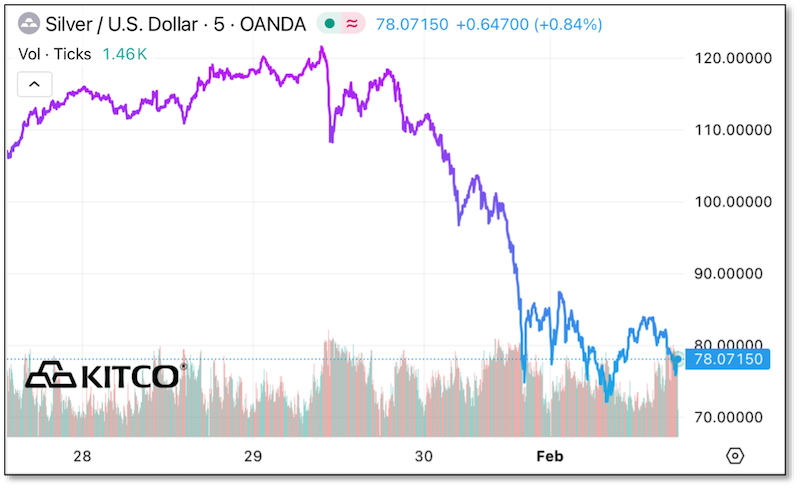

| Gold and silver were ascending so quickly that these markets were bound to trip over themselves. And so we’ve gotten this:

|

|

|

| From last Thursday to today, gold has shed about $1,000 and silver has plummeted about $50. On a percentage basis, this marks the sharpest decline in gold for 13 years and for silver...the steepest ever.

As you can see, the market has yet to reach equilibrium and margin-related selling as well as other features of the futures markets mean that it will probably take all of today, and perhaps tomorrow, for things to settle down.

I’ve included trading volume in the above charts to highlight how volume has spiked during the downdrafts. This indicates two things:

|

| 1) Traders are selling as their sell-stops get hit, and also piling on shorts to trigger those stops for other traders, and....

2) We have yet to see a rush of longs coming in to catch the falling knives.

|

| That latter should happen once the forced selling abates and that, as noted above, will take a bit more time.

There will be lots to discuss, unravel and discover over the days ahead, including the large premium for the metals in Shanghai, the record discount from NAV for the SLV silver ETF, and the possibility that this massive break in a broken metals market implies the failure of a major bullion bank.

For now, let’s examine the supposed trigger for this crash....

|

| The “Great Warsh-Out”

|

| Although gold and silver were tipping over in Asian trading on Friday, they were supposedly pushed over the brink by a very Western development: The decision by President Trump to nominate Kevin Warsh as Federal Reserve chairman.

Let’s get this straight from the start: The metals had already experienced a sharp drop in Thursday’s trading, although they had staged a respectable rebound by the end of the session.

Still, with massive long positions established (especially in Shanghai) on the metal’s torrid runs this year, and with hedges on longs that were essentially sell stops being set along the way, both markets were primed for toppling.

|

| Warsh’s nomination was simply one of many pins that could have popped this bubble.

|

| In fact, although Warsh was famously (and rightfully, in my mind) hawkish after the Great Financial Crisis and Covid, and an eloquent critic of quantitative easing, he has been spouting the party line of monetary easing since Trump’s election.

Make no mistake, that’s why he got the job.

Once in office, he will dutifully follow the implied instructions from the administration. And in fairness, political obligations are only part of the story. The simple mathematical fact is, he has no choice.

|

| With the U.S. federal debt at its current size, and with its unalterable trajectory, interest rates have to be lowered below the rate of inflation.

Otherwise, servicing of the debt becomes impossible, and the entire house of cards collapses.

|

| So Warsh was nothing more than an excuse. If it wasn’t for this, some other excuse would have sufficed at some point in the near future.

|

| Nothing Has Changed

|

| The essential truth behind all of this is that the fundamental factors of debt and depreciation — the “debasement trade” — remain firmly in place.

|

| We absolutely needed to Warsh-out the euphoria in metals, and this will give us a firmer base going forward.

|

| On that note, I expect that this pull-back will now help to bring out Western retail buying. The absence of that demand has been perhaps the most salient feature of this bull market.

The central bank-driven rise in gold surprised and shocked Western investors, leading professionals to delay their entry into the market and retail investors to simply sell into the sky-high prices.

Now they have a second chance, and one in which the underlying macro fundamentals are better understood.

I should also note that while gold stocks from the majors to the juniors leveraged the downward move on Friday, they aren’t doing too badly today.

In fact, one of the new junior mining stock recommendations that I unveiled Friday in our February edition of Gold Newsletter (a stock with I’m personally trying to buy today) is up over 12%!

Which brings me to my final comment:

|

| The underlying trend for the metals remains upward...and this correction has created some extraordinary, yet temporary, bargains.

|

| I strongly urge you to read this month’s hot-off-the-press edition of Gold Newsletter. I am confident that my top recommendations will be trading far, far higher a year from now.

And if you can act at this moment in time, at current prices, you could reap far greater rewards.

Click on the link below to get it all now.

|

| All the best,

|

|

| Brien Lundin

Publisher, Gold Newsletter

CEO, the New Orleans Investment Conference

|

| CLICK HERE

To Lock In A Full Year

Of Gold Newsletter

|

.png)