|

| When silver gets hot, most investors do the same thing they always do.

|

| They buy coins. They buy ETFs. They chase whatever already ran.

But the biggest gains in a real silver bull market rarely come from “owning silver.”

|

| They come from owning the companies that can re-rate as they move closer to production.

|

| And today, one U.S. asset-based developer — Apollo Silver (APGO: TSXV; APGOF: OTCQB) — looks like it was engineered for that exact re-rating.

|

| On Paper, It’s Already Huge

|

| Apollo is advancing Calico, a district-scale silver project in the historic Calico Silver Mining District in San Bernardino County, California.

This is not a one-vein wonder.

Under Apollo, the adjacent Waterloo and Langtry properties have been combined for the first time, outlining a district-scale mineralized system with about 6,000 meters of mineralized strike length and extensive historic drilling across the district.

Previous operators and Apollo drilled more than 52,000 meters across 541 holes at Waterloo and Langtry.

In other words: Much of the early-stage groundwork has been done. And the scale is real.

|

| The Second Largest Primary Undeveloped Silver Resource In The U.S.

|

| Apollo recently updated its mineral resource estimate for Calico with an effective date of June 30, 2025.

Here’s what that update says, in plain English:

|

| Waterloo now contains 125 million ounces of silver in 55 million tonnes at an average grade of 71 g/t silver in the Measured and Indicated categories at a cut-off grade of 47 g/t silver-equivalent.

Langtry increased from 50 million ounces to 57 million ounces of silver in 24 million tonnes at an average grade of 73 g/t silver in the Inferred category at a cut-off grade of 43 g/t silver-equivalent.[1]

|

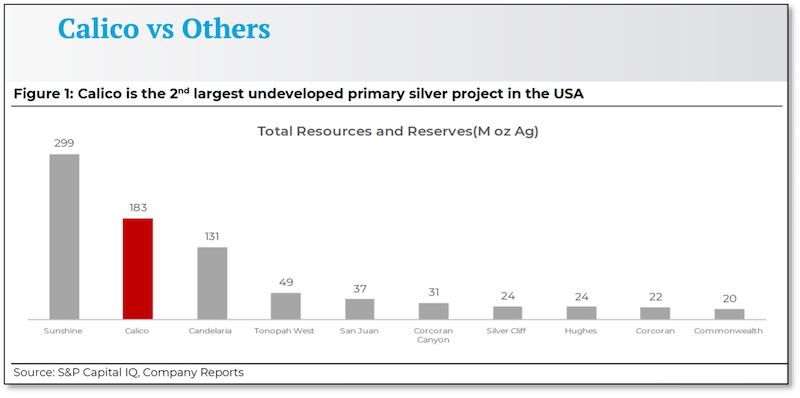

| That makes Apollo’s Calico project the second largest undeveloped primary silver project in the entire U.S.

Plus, there’s bonus potential in the Cinco de Mayo project in Mexico, also controlled by Apollo, that boasts a historical resource with 154 million ounces silver-equivalent at a grade of 385 g/t in the inferred category or 52.7 million ounces silver, 785 million pounds of lead, 1,777 million pounds of zinc and 96,000 ounces of gold in the inferred category.[2]

Subject to the granting of social license, completing the work necessary to make that large resource current could potentially add value to Apollo’s very large silver holding.

With all this silver, you would think Apollo would be among the most valuable silver stories in the nation, if not the world.

Well, not yet — but you’re about to see why that gap could close soon....

|

|

| Figure 1 - click image to enlarge

Apollo’s Calico project stands as the second largest undeveloped primary silver deposit in the entire U.S. — American silver, and lots of it, just when silver has been added to the U.S. list of Critical Minerals.

|

| The Silver Project With “Hidden” Value Most Investors Ignore

|

| Calico isn’t only silver.

Apollo also points to additional critical minerals at Calico, barite and zinc.

|

| And if you’ve been watching Washington, you already know why that matters: Silver itself was added to the U.S. Department of the Interior’s final 2025 USGS List of Critical Minerals.

|

| That designation completely changes the conversation around domestic supply.

It makes a large, undeveloped U.S. silver asset a very different kind of strategic story than it was even a year ago.

|

| The “No Help From Silver” Upside

|

| Yes, its large silver resource gives Apollo huge leverage to the price of silver.

|

| But here’s the part that should really make you sit up: Apollo could create tremendous value even if silver prices do nothing.

|

| That’s because this is one of those rare developer situations where the market is valuing the ounces cheaply today...and could be forced to pay much more later as the project de-risks.

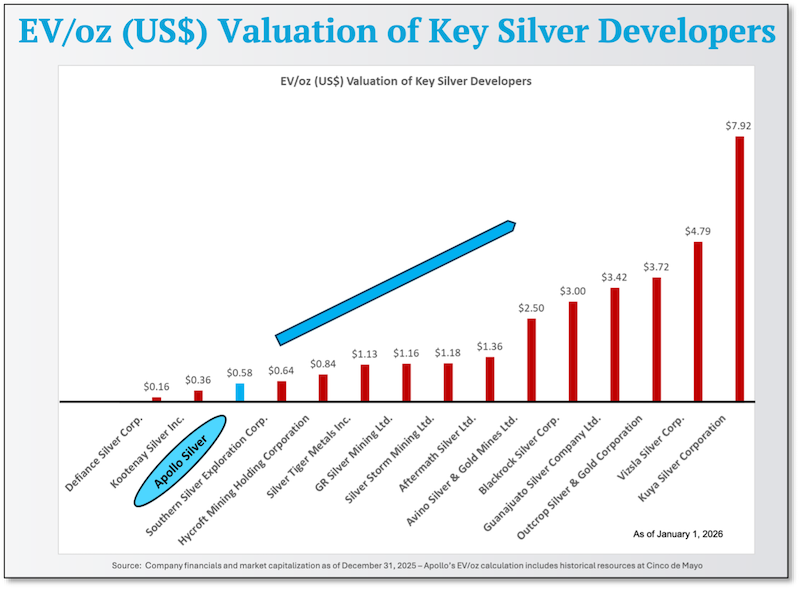

Consider this: Apollo’s enterprise value as of January 31 was approximately $190 million.

Compare that to roughly 125 million ounces of Measured and Indicated and 58 million ounces of silver at Calico, 154 million ounces of silver-equivalent at Cinco de Mayo and you’re talking about an enterprise value (EV) per ounce of only around $0.58.[3]

|

| That’s a small fraction of other silver plays at slightly more advanced stages.

|

| The kicker: That kind of valuation gap can close simply as Apollo continues to de-risk and advance Calico toward production.

Not a miracle. Not a takeover. Not a moonshot silver price.

|

| Just the steady march from “resource” toward “development-stage reality,” and a potential re-rating closer to where peer companies trade when projects get advanced.

|

| In a bull market, those re-ratings can be significant.

|

|

| Figure 2 - click image to enlarge

Apollo Silver is currently valued at just a fraction of the enterprise value per ounce of other silver companies...and that gap could close as Apollo simply advances the Calico project.

|

| The Catalyst Path Is Directly Ahead

|

| Apollo isn’t sitting still: The company has already outlined a 2026 exploration and development program at Calico that reads like a classic “advance the asset” roadmap:

|

| • A 4,500-meter HQ core drill program beginning in Q1 2026 to support metallurgical studies and geotechnical work for future mine design.

• Continued metallurgical test work through 2026, including efforts aimed at improving on recovery rates above the historical ~ 65% level.

• Early-stage permitting work, including baseline environmental monitoring, to start building the foundation for long-term permitting.

• Plus exploration drilling aimed at the Burcham gold expansion potential on the east side of Waterloo.

|

| And yes, there’s gold too.

Apollo notes Waterloo also contains 130,000 ounces of oxide gold in 17 million tonnes at an average grade of 0.25 g/t gold in the Inferred category.

Not the headline. But a helpful sweetener in a world where optionality matters.

|

| The “Smart Money” Signal

|

| All that work — all those key catalysts on the way to a potential re-rating — is financed.

|

| You see, Apollo just closed a $27.5 million private placement, including matching $12.5 million investments from Eric Sprott, and a fund managed by Jupiter Asset Management.

|

| That’s not a retail frenzy — that’s institutional-sized capital choosing to get involved while the story is still being built.

And it suggests Apollo has the kind of financial runway investors like to see when a company is stepping into serious development work.

|

| Why This Could Be the Ultimate Silver Play

|

| Put it all together and you get a setup that’s hard to ignore:

|

| • A large-scale U.S. silver resource in a mining-friendly part of California with infrastructure nearby.

• A clear, funded 2026 plan focused on drilling, metallurgical work, geotechnical and permitting foundations — all important de-risking steps working toward a potential re-rating.

• A low valuation-per-ounce that provides tremendous upside for a potential re-rating.

• A compelling opportunity for value creation through execution and continued alignment with peer group development stages.

|

| And that last point is the key.

Most investors only think you make money in silver stocks when silver rises...but developers can rerate on progress alone.

|

| When the market wakes up and starts paying “normal” dollars per ounce for an asset of this scale, the upside math can change fast.

|

| But in this business, the biggest moves often happen before that certainty arrives.

They happen when the market realizes the discount was the opportunity.

And that means this is the time to do your due diligence on Apollo Silver (APGO: TSXV; APGOF: OTCQB).

|

| CLICK HERE

To Learn More About Apollo Silver

|

| [1] For more information, please see the news release dated September 4 and October 16, 2025, and the N.I. 43-101 Technical Report titled “NI 43-101 Technical Report and Mineral Resource Estimate for the Calico Silver Project, San Bernardino County, California, USA,” dated October 16, 2025 (with an effective date of June 30, 2025). The Technical Report was prepared in accordance with National Instrument 43-101 (“NI 43-101”) Standards of Disclosure for Mineral Projects by Stantec Consulting Ltd. (“Stantec”) of Denver, Colorado. Mineral Resources are not mineral reserves and do not have demonstrated economic viability. There is no certainty that any mineral resource will be converted into a mineral reserve.

[2] An independent Qualified Person has not completed sufficient work to classify this as a current mineral resource or reserve and therefore the Company is not treating this historical estimate as a current mineral resource or mineral reserve. The reliability of the historical estimate is considered reasonable and relevant to be included here in that it simply demonstrates the mineral potential of the Cinco de Mayo Project.

[3] See Figure 2.

|

.png)