|

| Gold doesn’t have to “go up” from here to change the junior mining landscape.

|

| It already has.

The yellow metal is setting records every week and the fundamental factors driving this bull market don’t seem likely to let up for years to come.

In short...gold’s going higher. So how do we leverage that trend for maximum gains?

|

| Norsemont Mining Inc. (NOM.CSE, NRRSF.OTC) has figured out one particularly powerful approach.

|

| As you’re about to see, this company has figured out that the market is now rewarding a very specific kind of company: the one that can move from “resource story” to “cash-flow story” faster than everyone else.

|

| The Ready-Made Mine Story

Most Juniors Can Only Dream About

|

| Most developers spend years proving up ounces, then more years fighting their way through permitting and engineering, then they stare down capital expenses that can run into the hundreds of millions.

Simply put, Norsemont decided to sidestep all that.

|

| Instead of starting from scratch, it acquired a past-producing mine in northern Chile called Choquelimpie — a project with substantial existing infrastructure and a defined mineral resource base.

|

| Between 1988 and 1992, historical operators extracted 398,900 ounces of gold and 2.19 million ounces of silver from the high-sulfidation epithermal system at Choquelimpie. The mine didn’t close because it ran out of metal. It closed because the gold price environment back then didn’t justify continued operations.

Today, the environment is very, very different.

|

| A Resource Base With Real Weight Behind It

|

| Norsemont published an initial mineral resource estimate in April 2025 for Choquelimpie totaling 1.73 million indicated and 446 thousand in inferred gold- ounces, plus 33.2 million indicated and 7.2 million inferred ounces of silver.

|

| Those ounces are supported by extensive historical work, and the project’s metals mix is powerful in today’s market: gold leads...silver adds leverage...and copper provides optionality.

|

| This is one of those setups where the resource is big enough to matter, but the market still tends to categorize the company as “just another explorer” — at least until the next set of de-risking milestones begins to stack up.

And that’s where the infrastructure advantage comes in.

|

| A $175+ Million “Head Start”

|

| Choquelimpie comes with the kind of site profile that can change the entire development equation.

|

| Norsemont has highlighted existing infrastructure that includes power, water, road access, camp facilities and a 3,000 tonne-per-day mill. The company estimates that it would cost $175 million to recreate all that infrastructure.

|

| That’s a lot of money and time that’s eliminated from the equation. And that means less risk and much less dilution to shareholders as the project advances.

Not “no work required,” of course. But a very different risk curve than a greenfield build.

Norsemont’s strategy is straightforward and, importantly, sequential:

|

| First: Finalize a plan to process stockpiles and oxide material.

Then: Systematically drill and expand oxide and sulfide resources while also testing deeper copper porphyry potential.

|

| In a bull market, the companies that win attention aren’t always the ones with the wildest speculation. They’re often the ones that can show a credible path to a decision point...and then another...and then another.

|

|

| Click image to enlarge

|

| The Choquelimpie project is remarkable for the in-place infrastructure and multi-million-ounce gold resource, but the exploration upside along strike and at depth...and for copper...is also exceptional.

|

| The Fast Track Plan:

Oxides First, Expansion Next

|

| One of the most compelling elements at Choquelimpie is the idea of starting with the more straightforward material first.

|

| Norsemont is now building a geological model for stockpiles and in-situ oxides, defining metallurgical characteristics and assessing the existing plant and refurbishment needs.

|

| Metallurgy, plant condition and realistic restart cost estimates are the kinds of details that begin separating “good story” from “investable plan.” And Norsemont has been explicit that 2026 is about advancing engineering and feasibility work alongside drilling, environmental and metallurgical programs.

|

| Here’s What’s Coming Now…

|

| Norsemont ended 2025 with fresh capital and a busier 2026 calendar.

|

| In late December, the company closed a financing totaling approximately C$15 million (US$10.929 million principal amount in convertible debentures) and noted increased support from Crescat Capital alongside other strategic investors.

|

| Then, in early January, Norsemont provided its year-end update, outlining a clear set of objectives for the next 12 months: additional drilling (Phase 4 targeted for Q2), ongoing metallurgical work, a detailed report on plant condition and upgrade costs, a push into environmental impact assessment work, and later-year goals that include an updated resource estimate and a PEA focused on oxide production plans.

That’s the kind of cadence the market can follow...and start to price in.

|

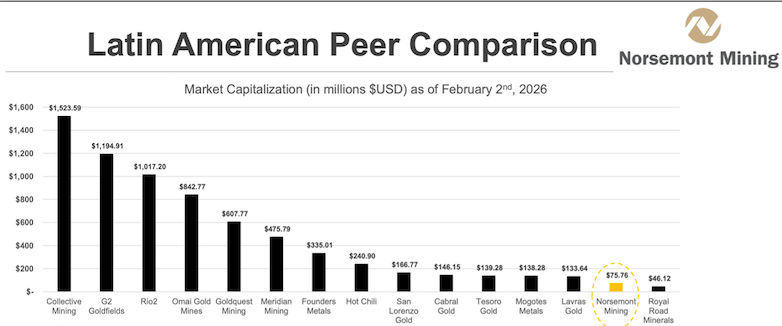

| |

| A comparison to Norsemont’s peer group shows how far the company can go by simply continuing to advance and derisk its Choquelimpie project.

|

| Powerful Optionality With Copper And More

|

| There’s another element to Choquelimpie that serious resource investors tend to appreciate: the deposit style.

You see, high-sulfidation epithermal systems can run deeper than what early-stage operators historically chased, particularly when the focus was on near-surface, heap-leachable material.

|

| Norsemont has been transparent that part of its plan is to drill deeper high-grade targets using historical data to grow the sulfide resource, while also assessing deeper copper and gold porphyry systems below the sulfide gold mineralization.

|

| In other words, there’s a base case (oxide processing and a restart plan) and there’s upside (resource expansion and deeper system potential).

You don’t need to assume the upside to see why this is interesting. But if the upside begins to show up in the drill bit and the models, it could change the ceiling...and the company’s market value...quickly.

|

| A Team Built for the “Do” Phase

|

| When a junior transitions from the “tell” phase to the “do” phase, execution becomes everything.

Norsemont has been adding technical and operational depth, including key leadership appointments and Chile-focused expertise.

|

| In its January update, the company highlighted expansions across geology, environmental permitting and finance, as well as the engagement of firms for metallurgy, drilling approvals and plant assessment work.

|

| That’s exactly what you’d expect to see from a company that’s trying to move faster than the typical development timeline.

|

| Why This Matters Right Now

|

| When gold is stuck in the $1,700–$2,000 world, a restart story can feel like “someday.”

When gold is trading around $5,000, “someday” starts looking a lot more like “soon”...or even “now” — especially for past-producing assets with infrastructure already in place.

Norsemont’s pitch, at its core, is simple:

|

- A past-producing Chilean gold-silver mine

- A defined resource base in the millions of gold-equivalent ounces

- Existing infrastructure that can compress time and cost

- A 2026 work plan built around drilling, metallurgy, engineering and permitting milestones

- And a market backdrop that makes every month of progress matter more than it did a few years ago

|

| In this kind of market, stories can rerate quickly once the “next step” becomes visible.

That’s why Norsemont is worth a close look now, while it’s still in that transition zone between “resource story” and “restart trajectory.”

|

| CLICK HERE

To Learn More About Norsemont Mining Inc.

|

.png)