|

Earnings season has come and gone. Mixed results but fortunately for us, we’ve largely seen steady margin increases as companies seek to maintain a tight grip on inflation while working toward increasing production.

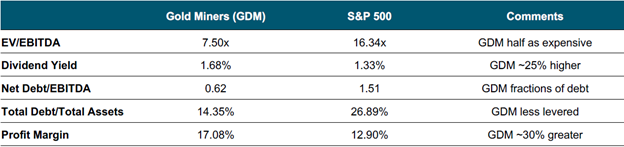

If you have any questions about individual companies in your portfolio, please reach out. Since the start of the year, there have also been many other company updates worth discussing. In fact, as I write I am on my way back from having attended the PDAC mining conference in Toronto. A useful time to put your ear to the ground, catching up with going concerns as well as other industry professionals. If you’d like a quick debrief, feel free to call. I am making a quick pit stop in San Diego before returning to New York, to debrief with the investment team in Carlsbad. They have recently returned from the BMO mining conference in Miami. From preliminary reports, it was productive and encouraging… Whisper it quietly, larger generalists are turning up in the precious metal space… I am in the middle of a busy travel schedule. Two weeks ago, I was in Nicaragua checking in on things, this week I was in Toronto and next week I will be attending the Swiss Mining Institute (SMI) investment conference in Zurich, where I am speaking on a panel. If you will be attending the SMI conference in Zurich, I would love to meet up so please let me know ahead of time. I hope to see some of you there. I wanted to spend some time today unpacking the flurry of macro news and subsequent volatile market activity. Tariffs are obviously taking center stage as Trump’s 25% tariffs on Canada and Mexico (now exempt until April 2nd) and 20% tariffs on China (up from 10%) took effect overnight, affecting $1.5T of annual imports. Canada responded with 25% tariffs on C$30B of U.S. goods with an additional C$125B of U.S. imports slated for tariffs in three weeks. While China retaliated with 15% on U.S. agricultural goods (effective March 10) and banned exports to various U.S. defense companies. While the first order effect is to restrict the flow of vital commodities, and perhaps boost domestic supply, it will take time to bring additional production and manufacturing online. Copper was up over 5% in the first hours of trading on Wednesday. This kind of volatility for big markets like copper is rare and unstable. Remember Newton’s Third Law: for every action, there is an equal and opposite reaction. Restricting free trade is hardly ever a driver of economic prosperity. Paul Wong, Sprott’s Market Strategist, is on the case: economic data continues to weaken while inflation readings are elevated and sticky. For all the economic uncertainties, sadly one constant remains. War. “We are in an era of rearmament” declared Ursula von der Leyen, president of the European Commission, after announcing plans for $158B in loans to boost defense spending and a mechanism to allow EU countries to spend an additional $685B on defense over four years without triggering budgetary penalties. Governments also have plans to keep spending big on energy infrastructure. In fact, total expected grid capacity is set to increase over 400GWh in 2025, that’s up from 160GWh last year. So, despite the current sentiment of economic woes, it might be worth looking at some undervalued critical materials. Uranium would not be a bad place to start considering the current disconnect between the spot price and long-term contracts. Megatons for Megawatts notwithstanding, the price seems to have found a fundamental floor, right around the incentive price for new production. Meanwhile nuclear adoption is showing no sign of slowing down… I digress, I wanted to touch on gold and its miners – arguably a safe harbor in this mess. I don’t think you can say the same of bitcoin yet, I’m afraid. Our investment team recently put these charts together to highlight the investment case for gold mining equities. These still trade as if there is no commodity price upside, often below 1x Net Asset Value, well below S&P 500 valuations. And these businesses are demonstrably more sound in terms of debt to earnings, dividend yield (to be honest that one surprised me), and overall profit margin. |

| Source: Bloomberg as of 9/30/2024. Gold Miners (GDM) represents the NYSE Arca Gold Miners Index (GDM INDEX). |

| The following chart shows how gold mining equities have been substantially underperforming gold so far this cycle. With western retail investors potentially starting to come back in the trade, this could change dramatically. |

| Source: Bloomberg and FactSet as of 12/31/2024. |

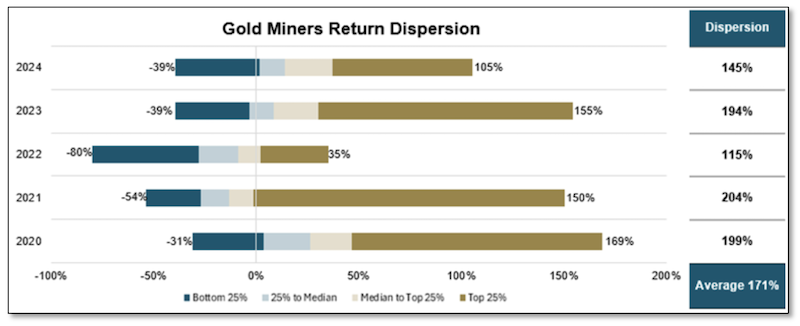

| In the meantime, gold continues to gain favor from central banks. PRC Macro is forecasting that the PBOC will purchase 400t of gold this year, compared to just 40t in 2024. For reference, central banks added a total of 483 tonnes of gold in the first half of 2024. Needless to say, China’s increased buying would be very meaningful for the gold sector. When I talk to investors, lamenting the gold equities’ performance relative to gold, they tend to point to the GDX, and some of the larger cap constituents of the ETF. While it’s definitely not a good look to have the two largest gold miners underperform so badly, and rightly so thanks to their poor operational performance to date, the return dispersion has been very wide year-over-year. |

| Source: Bloomberg and FactSet as of 12/31/2024. Gold Miners represent the GDMNTR and the constituents of GDX ETF, which tracks GDMNTR. |

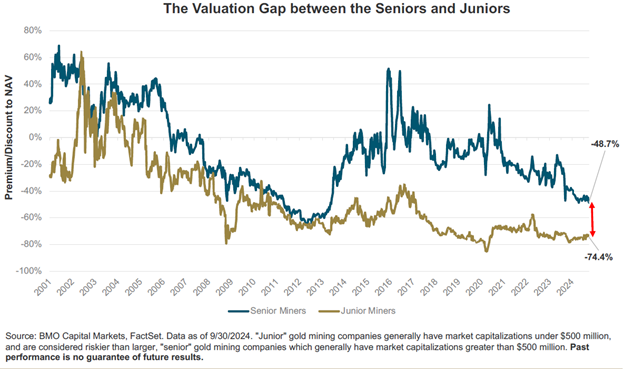

| And based on the valuation gap between seniors and juniors, still plenty of room to go. |

| Source: BMO Capital Markets, FactSet. |

| That is all I have for you today. I keep thinking of Robert Friedland’s quote: “It’s the revenge of the miners.” Down for so long, it might be time for commodities to take center stage. Please feel free to reach out if you have any questions. Regards, Edward P.S. If you need help with managing your portfolio of mining equities, please reach out for a free consultation. Edward Bonner

Investment Advisor, Geologist Sprott Global Resource Investments Ltd.

1910 Palomar Point Way, #200

Carlsbad, CA 92008 ebonner@sprottglobal.com |

| Important Disclosure Relative to other sectors, precious metals and natural resources investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered. Gold and precious metals are referred to with terms of art like store of value, safe haven and safe asset. These terms should not be construed to guarantee any form of investment safety. While “safe” assets like gold, Treasuries, money market funds and cash generally do not carry a high risk of loss relative to other asset classes, any asset may lose value, which may involve the complete loss of invested principal. Past performance is no guarantee of future results. You cannot invest directly in an index. Investments, commentary, and opinions are unique and may not be reflective of any other Sprott entity or affiliate. Forward-looking language should not be construed as predictive. While third-party sources are believed to be reliable, Sprott makes no guarantee as to their accuracy or timeliness. This information does not constitute an offer or solicitation and may not be relied upon or considered to be the rendering of tax, legal, accounting or professional advice. |

.png)