|

| Not long ago, Mt Todd was considered a “someday” project.

|

| The grade was a little low. The initial capex was a little high. And gold wasn’t quite high enough to make it scream.

All of that has changed.

|

| Vista Gold (VGZ.TO; VGZ.NYSE-A) has right-sized Mt Todd into one of the most compellingly economic gold projects available for development anywhere in the world.

|

| And with gold trading around $4,500 per ounce, the numbers are nothing short of extraordinary.

|

| What Makes Mt Todd Different Now

|

| Vista Gold’s 2025 feasibility study wasn’t just a technical update. It was a fundamental rethinking of how to unlock Mt Todd’s value.

|

| |

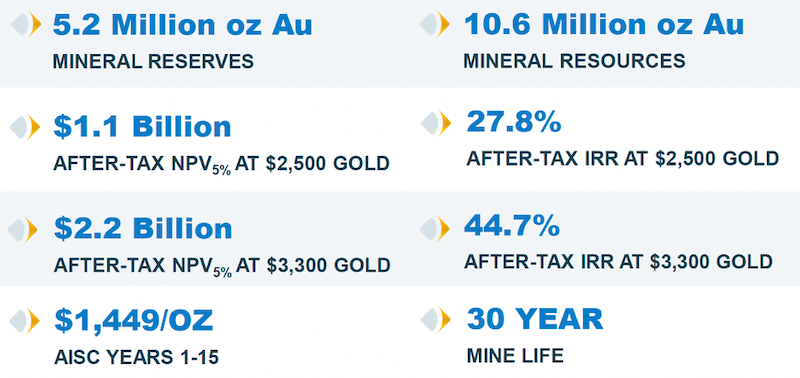

| Vista Gold’s new feasibility study shows exceptional economics — plus outstanding leverage to the gold price.

|

| Vista raised the cut-off grade from 0.35 to 0.5 g/t, to get the average gold grade for the mine over 1.0 g/t for the first 20 years of operation. That’s just one of the conservative decisions that boosted the economics.

The lower-grade material between 0.35 and 0.5 g/t, roughly one million ounces, won’t be lost, but stockpiled for future processing. That’s another potential boost.

The result is a 15,000-tonne-per-day operation producing approximately 150,000 ounces of gold per year at a grade competitive with some of the largest open-pit mines in Australia, with a manageable $425 million initial capex.

|

| And the economics were built on a deliberately conservative gold price assumption of $2,500/oz.

At $3,300/oz., the leverage to the gold price is remarkable. At today’s prices...the numbers are nothing short of staggering.

|

| Still Huge Optionality For A Major

|

| Here is what makes Mt Todd genuinely unusual even among large development projects.

The 15,000-tonne-per-day design is sized for Vista to develop on its own. But the same deposit could support a 500,000-ounce-per-year mine if a major mining company wanted to scale it up.

The resource base of over 10 million ounces is there. The infrastructure corridor is there. The jurisdiction is world-class.

In short, what was once considered an optionality play has evolved into one of the few gold projects on earth that can truly move the needle for a major producer.

|

| Not many 10-million-ounce projects offer such robust economics at today’s gold prices, a clear development path and obvious room for much further growth.

And even fewer are located in a jurisdiction as friendly to mining as Australia.

|

| In short, any serious list of M&A targets for the world’s top gold producers would have to include Mt Todd near the top.

That gives Vista three very distinct paths to value creation:

|

| The company can develop Mt Todd independently.

...It can attract a joint venture partner to develop the project at a much larger production rate...

...Or it can be acquired outright by a major at a significant premium to current prices.

|

| Vista is fully in control of its destiny, whichever path the market delivers.

|

| De-Risking, Box By Box

|

| For investors, buyers and potential partners, Vista is methodically removing every remaining reason to hesitate.

The work underway includes:

|

- An update of the project’s permits and authorizations to align with the new mine plan, with all approvals expected in due course given that the same permits have been granted before for a larger footprint

- Metallurgical and geotechnical drilling programs underway to optimize mine design, confirm recoveries and provide data for equipment selection and sizing

- A growing Australian-based executive team being assembled to lead the project through development

- Active project execution planning to position Mt Todd for the start of detailed engineering and design

|

| These are programs in progress, with a management team that has done this before and the funding to see it through.

|

| Backed By Serious Capital

|

| The market’s confidence in Vista’s plan was on full display this past March.

Vista closed an underwritten public offering of about $45 million at $2.50 per share on March 9th, with underwriters exercising their full overallotment option.

|

| The offering was heavily oversubscribed, a strong signal that sophisticated institutional investors are lining up behind this story with conviction.

That same smart money was willing to pay $2.50 per share — much more than you have to pay now.

|

| Vista now carries no debt and holds over $55 million in cash, giving it the runway to build the Australian team, complete the permitting modifications and initiate detailed engineering and design.

|

| The Opportunity In The Valuation Gap

|

| All of the above is unfolding against a backdrop of a Mt Todd NPV that dwarfs Vista’s market cap by a very wide margin.

The 2025 feasibility study puts Mt Todd’s after-tax NPV at $1.1 billion at the conservative $2,500/oz. base case. At $3,300/oz., that figure doubles to $2.2 billion. At today’s gold prices near $4,500/oz. — the value of this deposit is in another league entirely.

And Vista’s current market cap? Still below $300 million.

|

|

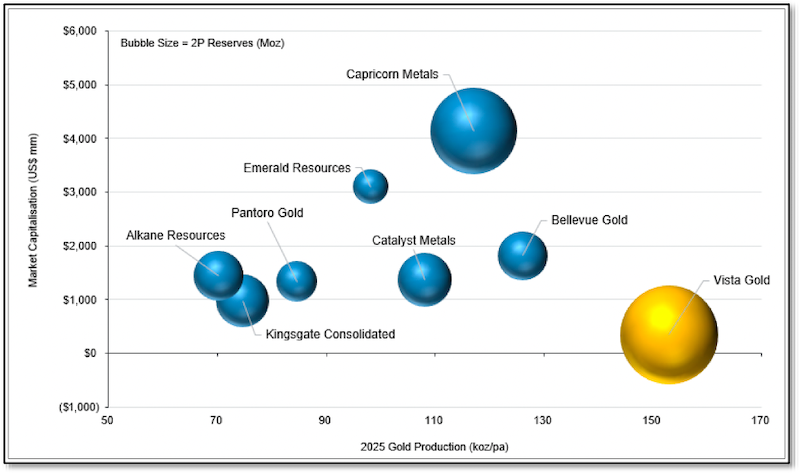

| Vista Gold’s market cap fails to reflect its expected production, especially compared to those of its Australian peers.

|

| In the midst of the greatest gold bull market investors have ever seen, Mt Todd stands out as one of the largest, most advanced and most compellingly valued development projects in the world.

For investors looking for the ultimate gold bug play, Vista Gold deserves a very close look now...at this crucial moment in its development and valuation.

|

| CLICK HERE

To Learn More about Vista Gold Corp.

|

.png)