|

| How do I make the most of this gold bull market? |

| In the wake of a generational run in prices for the yellow metal, it’s a question that’s on every gold bug’s mind. |

| If history is any guide, the answer will be found in the junior sector, which tends to offer the most leverage to gold as a bull market accelerates. |

| In particular, companies with a large bank of gold in the ground can see the value of that resource drive its share price sky high, as higher gold prices make even moderate-grade projects increasingly profitable. |

| That description fits Mayfair Gold (MFG.V; MFGCF.OTC) to a tee. |

| Its Fenn-Gib project within Ontario’s portion of the prolific Abitibi Greenstone Belt has a large, indicated gold resource and a path to production that will bypass Canada’s lengthy federal mine approval process.

Mayfair Gold’s plan is simple: Get a profitable, open-pit gold mine in production as fast as possible, thereby offering investors leverage on historically high gold prices. |

| Fenn-Gib:

4.3 Million Ounces Of

Indicated Gold Perfectly Located |

| While some gold equities are bets on discovery, Mayfair Gold is very much a company with an established resource.

Fenn-Gib has seen a remarkable 300,000 meters of drilling over its history and fully 97% of its resource is in the indicated category (4.3 million ounces). |

| |

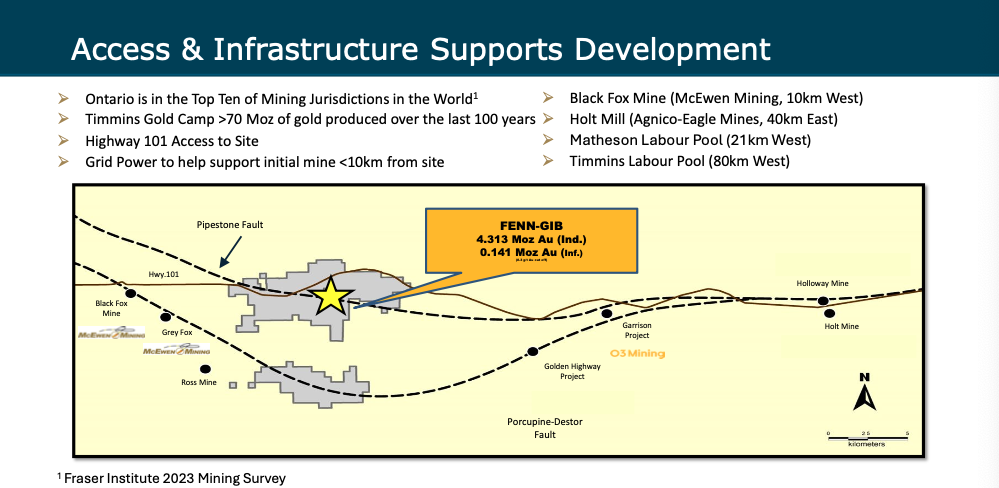

| Click image to enlarge Fenn-Gib’s Abitibi address gives it access to a wealth of mining infrastructure. |

| Thanks to its Abitibi address, Fenn-Gib has excellent access to infrastructure. Highway 101 runs near the project, and available power is just 10 kilometers to the west, as are the mining towns of Matheson and Timmins. |

| Ontario is one of the safest mining jurisdictions in the world, and its Timmins Gold Camp has produced more than 70 million ounces of gold over the last 100 years. |

| Fenn-Gib is a project with a large gold resource that seems destined to become a mine, given gold’s current trading levels. |

| A Plan To Fast-Track Production |

| And management is level set on putting a mine at Fenn-Gib into production during this gold cycle. |

| To do so, it has developed a scaled plan for production that will allow it to start production through a provincial mine approval process, rather than the lengthy federal mine approval process. |

| That plan involves a mine that would operate at a 4,800-tonne-per-day level — large, but just below the threshold for a mine that would require federal permits.

The provincial rules that will apply instead will result in a much faster permit approval timeline — one year as opposed to seven years for an environmental permit...and three years as opposed to 10 years or more for a mining permit. |

| |

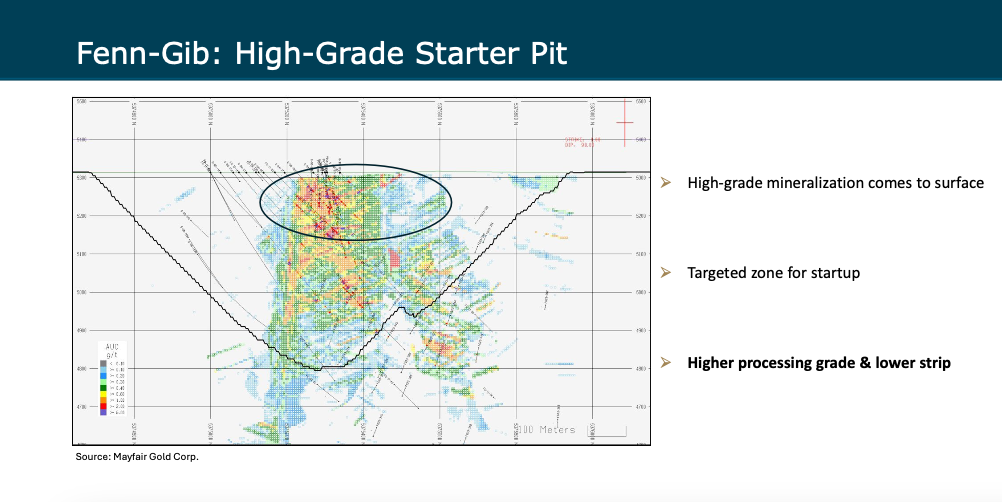

| Click image to enlarge The circled area on the Fenn-Gib map above highlights a potential starter pit that could allow for rapid capex payback. |

| Supporting this fast-track to production is a higher-grade starter pit within Fenn-Gib that will let Mayfair quickly pay back the mine’s capital costs.

This plan will result in reduced up-front capital, time to production and risk to shareholders, and it will allow the company to convert this cycle’s high gold prices into rich cash flow. |

| Determined To Deliver Leverage |

| Fenn-Gib’s indicated resource has an average grade of 0.74 g/t.

In a lesser gold market, that grade would be marginal for an open-pit operation.

In today’s market, however, that resource could be hugely profitable, especially given its Ontario location and the mineralization’s favorable recovery levels. |

| In other words, that marginal profitability means the project becomes a source of potential leverage for Mayfair Gold’s share price. |

| Management’s plan is to monetize Fenn-Gib’s resource as quickly as possible and then to hold a portion of the gold it produces to provide even greater exposure to higher prices.

It’s a “hold your gold” strategy designed with gold bugs very much in mind. |

| CEO’s Past Experience Offers

A Roadmap To A Re-Rating |

| So, what’s the upside at Mayfair Gold?

Well, for clues, one should look at the two previous companies where CEO Nick Campbell worked: Artemis Gold and SilverCrest Metals.

During his stints at both companies, they put mines into production. |

| Artemis Gold had a C$400 million market cap at the start of Campbell’s time there. Fast forward today, and Artemis is in production and sports a market cap around C$4 billion.

SilverCrest was trading at just a C$15 million market cap when he started there. By the time he left in 2020, SilverCrest sported a C$1.5 billion valuation. It would go on to get bought this year by Coeur Mining for C$2.2 billion. |

| The Artemis Gold example is particularly relevant in Mayfair Gold’s case.

As Mayfair is doing at Fenn-Gib, Artemis took a staged approach to getting its Blackwater project into production, thus allowing it to start turning Blackwater’s ore into cash flow in this cycle. |

| In an M&A market where cash-rich producers are looking for resources and reserves to add to their portfolios, Mayfair Gold and its massive Fenn-Gib project — in the midst of the Timmins gold camp — stand out as a premier takeout target. |

| Simply put, if you’re looking for leverage on gold, you need to be taking a close look at Mayfair Gold now. |

| CLICK HERE

To Learn More about Mayfair Gold |

.png)