Royalty companies are generally the first names off the shelf when generalist investors begin rotating into gold en masse.

|

These companies’ ability to generate cash flow off higher gold prices without much of the risk and costs associated with operating a gold mine makes them very attractive.

Of course, there is a flip side to the leverage these plays offer — you have to think ahead if you want to maximize your gains.

|

If you wait until gold prices begin to move, rapid gains in royalty companies can easily outrun your ability to fully leverage the trend.

|

That’s what makes the recent price discount the market has applied to Vox Royalty Corp. (VOX.V; VOXCF.OTC) so tantalizing.

Here we have arguably the most aggressive player in the sector in terms of portfolio growth, and it’s trading below the levels of a recent financing.

That’s because one long-short hedge fund participant in the financing — among a roster of otherwise committed longs — decided to quickly exit its position, a move that has put Vox unexpectedly on sale.

But bargains in this space have a way of vanishing quickly, making now a near-ideal time to take a closer look at Vox.

|

Royalty Companies: Hard To Beat For Leverage

|

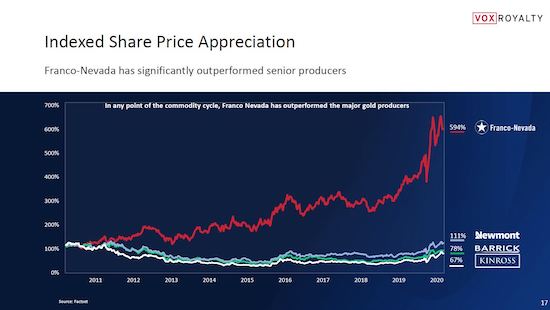

To understand why royalty companies are so sought after in gold bull markets, take a look at the chart below, which compares the returns of Franco Nevada, the royalty sector leader, versus the returns of some of the sector’s major gold miners over the past decade.

|

|

|

Granted, Newmont, Barrick and Kinross all turned in nice gains in 2020 during gold’s big run after the initial market-wide crash last March from the Covid lockdowns.

But Franco Nevada blew its operator competitors away during that period, besting these companies’ returns by five times or more.

Why?

Because royalty and streaming companies are arguably the best way to invest in the mining industry. These plays:

|

• Offer great leverage on commodity prices

• Typically generate strong margins

• Have fixed operating and cash costs, with no capex or cost overrun exposure

• Have no limit to growth based on project execution risk

• Provide exposure to exploration upside essentially for free

|

That’s a potent combination of benefits, and Vox Royalty possesses every single one of them.

Plus, it has been maintaining the sector’s most aggressive pace in terms of deal flow.

Save

Not A Subscriber Yet?

Get Golden Opportunities For Free

Subscribe to our Golden Opportunities e-letter to receive timely market

updates from the Gold Newsletter research team, plus video

presentations by expert speakers from the New Orleans Conference

— and the Investor’s Guide to Gold and Silver — all at no cost!

CLICK HERE to start your subscription.

|

Vox’s Aggressive Deal Flow Pace Continues

|

The team at Vox has kept up that pace since last month’s financing, a C$16.9 million overnight marketed public offering.

That financing is what created the short-term share price weakness that’s providing investors with such a compelling entry point for Vox.

It has also given the company funds to stay active on the acquisition front, and Vox has put the money right to work, with deals that add to its leading royalty portfolio position in Western Australia, including:

|

• A $0.50/tonne royalty on the producing Janet Ivy mine and a 2.5% net smelter return on the Otto Bore project for total consideration of A$7 million.

• A $10/oz. royalty on the three-million-ounce Bullabulling gold project for $2.2 million in cash and shares.

• A $1.78 million payment to extinguish a third-party-held royalty pre-payment due on the Koolyanobbing mine, a move that will allow Vox to begin collecting its own royalty revenue from the project immediately.

|

As you can see, all three deals have the potential to boost Vox’s near-term cash flow — a closely watched metric for royalty plays.

|

Now Trading At A Discount To Peers

|

These latest transactions add to no less than 47 royalties and streams Vox already had in its portfolio, 80% of which are in areas of low geographic risk (i.e., Australia, Canada and the U.S.).

|

Simply put, no other royalty company out there compares with Vox in terms of growth via acquisition — it has completed more than 20 transactions since January 2019.

|

Of course, even more important than the number of royalties is their quality.

And yet, Vox is getting nowhere near full credit for the quality of its assets or its steep growth profile, as the following Price/NAV comparison of royaltycos makes clear.

|

|

|

As you can see, just to get to the average level enjoyed by some if its peers, Vox shares would need to more than double from their current levels.

|

This Ground Floor Entry Point Won’t Last

|

The bottom line is this: The recent weakness in Vox’s share price is making the company a must-own bargain if you want to leverage gold’s next big run.

|

Almost all gold stocks did well in the post-lockdown surge in precious metals in 2020 — but royalty plays as a group spiked faster and delivered much more leverage.

|

With the flood of stimulus that continues to pour into a global economy primed for a post-vaccination recovery, the table is set for higher gold prices in the near future.

That means this sale on Vox Royalty isn’t likely to last long…and those who take advantage now will likely be handsomely rewarded.

|

.png)