Trends towards healthy eating and sustainability have made organics one of the food industry’s fastest growing and most lucrative sectors.

|

Millennials and Gen Zers, in particular, have an increasing desire to know where their food comes from, what its nutritional profile is, how it was raised or cultivated and how it got to them.

|

Proof of the growing popularity of organics can be seen in the absolutely explosive growth rate for the sector.

|

In an industry better known for growth rates in the low single digits, the organic food and beverages sector is set to post a compounded annual growth rate of 14.5% between 2017 and 2024, according to Zion Research.

Such powerful growth and healthy margins are what drew Organto Foods (OGO.V; OGOFF.OTC) to the organic space. They’re also what helped propel the company to as much as an eight-fold share price gain over the past year.

But these tantalizing gains are likely just a taste of what’s to come for Organto, as the company is only now hitting the steep side of its growth curve.

|

Organic Trend Shows No Signs Of Slowing Down

|

Organto’s focus on organically sourced fruits and vegetables puts it squarely in the largest category within the organic sector.

As of 2018, there were 2.8 million organic producers in the world, a 55% gain since 2009.

Growers of organic fruits and vegetables account for 71.5 million hectares of the world’s farmland, with 186 countries engaged in some form of organic farming.

|

|

|

Organto’s geographic focus is currently on the EU, where organic fruits and vegetables represent a €10.7 billion, and growing, market.

Organto’s goal: To increase its EU market share (currently at less than 1% of the specialty market) to 5% of the total category — a C$800 million revenue opportunity.

|

Driven By Two Strong Tailwinds

|

Two key trends are putting the wind at Organto’s back as it sets its sights on this ambitious goal.

First, a regulatory shift toward more healthy and sustainable foods systems in the EU is part of the trading block’s broader “European Green Deal.”

One prong of that effort calls for organic farming to account for fully 25% of the EU’s farming sector by 2030, a steep increase from the 8.5% share it held in 2019.

Even if the EU only gets halfway to this mark, it will create a world of opportunity for Organto, which is always looking for nearby sources for its products.

|

|

|

And then there’s Covid.

As we all well know, the pandemic and its lockdowns have forced vast shifts in consumer eating habits, with an increase in home cooking and a growing emphasis on health.

Fully 22% of consumers say they’re eating healthier since the pandemic started, driven by a desire to bolster their immune systems.

And 47% plan to cook more often when the pandemic is over.

Simply put, there is likely to be a significant long-term shift to home cooking post-Covid and an increasing demand for healthier food options.

It’s a confluence of events that Organto Foods, with its scalable, asset-light business model and emphasis on branded products, is set up to leverage to the hilt.

Save

Not A Subscriber Yet?

Get Golden Opportunities For Free

Subscribe to our Golden Opportunities e-letter to receive timely market

updates from the Gold Newsletter research team, plus video

presentations by expert speakers from the New Orleans Conference

— and the Investor’s Guide to Gold and Silver — all at no cost!

CLICK HERE to start your subscription.

|

Asset Light Model + Branding Focus = Robust Margins

|

Under this model, Organto doesn’t own the asset-intensive farms or processing facilities that produce its organic fruits and vegetables…

…It owns the supply chain.

It’s a model that lets growers do the growing and processors do the processing while the company focuses on growing its global, geographically diverse roster of suppliers.

This model is also very capital efficient. The Organto team estimates it needs just C$1-$1.5 million to generate each additional C$10 million in revenue.

|

And between that scalability and its branding initiatives, Organto is set to grow very, very profitably in the years ahead.

|

Management is especially excited about its “I AM Organic” initiative.

|

|

|

Currently in its pilot phase, this initiative features minimal packaging and a QR code that consumers can scan to quickly see that fruit or vegetable’s “digital passport.”

With branded products offering margins as high as 20%-40% (as opposed to 8%-12% for bulk/distributed products), success with this program has the potential to super-charge Organto’s profitability.

|

Targeting C$100 Million By Next Year

|

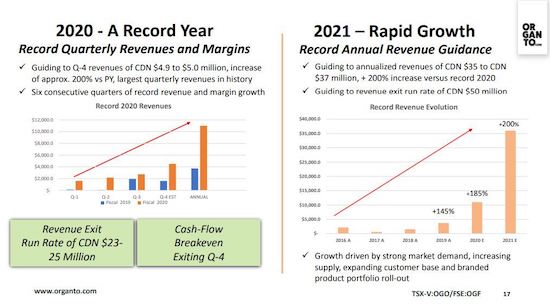

Those robust margins are set to occur even as Organto fully expects to grow its exit run-rate to $C50 million in 2021 with the objective of an exit run-rate of C$100 million by the end of 2022.

That steep growth profile will come on the back of six straight quarters of record revenue and margin growth.

As the graphic below demonstrates, Organto projects it exited Q4 2020 with a run-rate between C$23 million and C$25 million, with full-year revenues expected to have grown around 185% to C$11.5 million.

|

|

|

Management guidance for 2021 forecasts another 200% in growth, with C$35 million to C$37 million of revenues for the full year and an exit run-rate of C$50 million.

And Organto is targeting revenues to double yet again in 2022, ending the year with that aforementioned C$100 million exit run-rate.

|

These aren’t pie-in-the sky estimates — as a supply chain company, Organto knows what’s in its pipeline well before new sources of supply hit the market.

|

They are also very likely conservative, as they account only for internal growth.

Organto plans to take every opportunity to grow via acquisition as well, as it seeks to roll up a fragmented EU market.

|

A Compelling

(And Likely Fleeting)

Window Of Opportunity

|

Opportunities to invest in companies that combine strong top-line growth with compelling margins don’t come along every day.

In Organto, Chairman and Co-CEO Steve Bromley sees an early-stage version of SunOpta, the food company he joined in 2001 and grew to approximately C$1.4 billion in revenue over his 15-year tenure.

In fact, the chance to build SunOpta 2.0 was so enticing, SunOpta’s founder (and former Chair and CEO) Jeremy Kendall has joined Organto’s board, as has former SunOpta executive and founding director Joe Riz.

With Organto’s scalable, asset-light business model and the trends for organics very much on its side, these food industry veterans see a real chance to match (or even exceed) SunOpta’s performance.

|

And despite the eight-fold gain Organto Foods has posted in the past year, its shares are still trading at a deep discount to its forecasted revenue and margin growth.

|

But a growth curve this steep built on consumer trends this obvious means Organto’s current bargain levels will likely have a short shelf-life.

If you like the organic story, you’ll want to take advantage of this (fleeting) window of opportunity to leverage it by owning Organto Foods, before its steep growth profile makes it a true market darling.

|

.png)