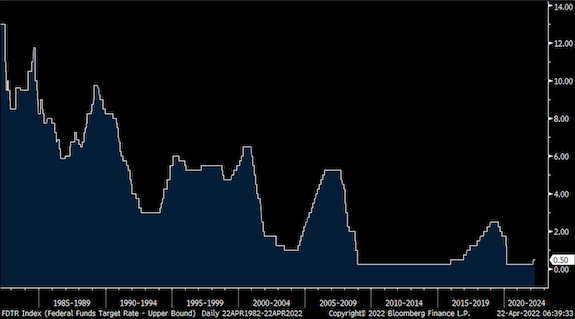

| Since the early 1980s, each rate hiking cycle ended below the peak of the prior one.

In Q4 2018 the Fed stopped when the fed funds rate got to 2.25-2.5%. So, the rather quick pace and much higher level of rate hikes currently priced in, 50 bps at each of the next three meetings, an ultimate near 3.5% fed funds rate by next summer and an annualized pace of QT of $1.14 trillion, would be by far the most aggressive tightening stance seen in a post Volcker world if the Fed actually follows through.

And it won’t just happen in a vacuum in order to tame inflation. Decades of easy money have medicated an entire economy on a low cost of capital and given markets reason to achieve ever higher multiples and ever tighter credit spreads. It is why the investing world has changed this year and why the coming few years will be quite different than the previous.

While investing has seemed “easy,” it never is and now is ever more difficult and challenging. With the S&P 500 still trading at 19x earnings, the NASDAQ by 27x, the Bloomberg high yield index spread to Treasuries of 344 bps vs the 10-year average of 435 bps and 20-year average of 510 bps, there is just no room for error here. Own short-term Treasuries at current yields, avoid long duration. Own dividend-paying value stocks. Own commodity stocks still, especially energy and precious metals. Own the local currency bonds of emerging market commodity currencies that have great yields. And don’t be afraid to buy cheap stocks in Asia and Europe.

And keep in mind that trillions of dollars of loans are LIBOR/SOFR based. If you didn’t see...the (recent) WSJ article titled “Floating rate debt bits corporate loans,” the article says “The benchmark rates that most leveraged loans are priced off are expected to rise to around 3% in the next 12 months, from about 0.50% now, according to Citigroup research. That equates to a $45 billion interest expense increase on the loans that were issued in 2021 alone, according to Dealogic data...Companies are more exposed than during the previous LBO boom in 2007 because most loan investors no longer require them to purchase derivatives to hedge against rising rates” according to a Citi strategist.

I mentioned a few months ago the retail money that flooded into floating rate funds/ETFs hoping to benefit from rising short term rates without doing the credit work on the companies that have this floating rate debt.

Fed Funds Rate

|

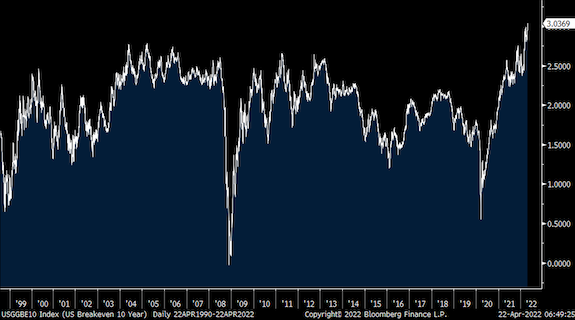

| Notwithstanding all the tightening expected to come, it has done absolutely nothing to quell inflation expectations in the TIPS market. (Recently) the 10-year inflation breakeven closed above 3% for the very first time at 3.04%, dating back to 1998. The 5-year...closed at 3.63%, matching a high. Also of note, the 5-year/5-year inflation rate, so years 6 through 10, is at the highest since 2014 at 2.63%.

10-Year Inflation Breakeven

|

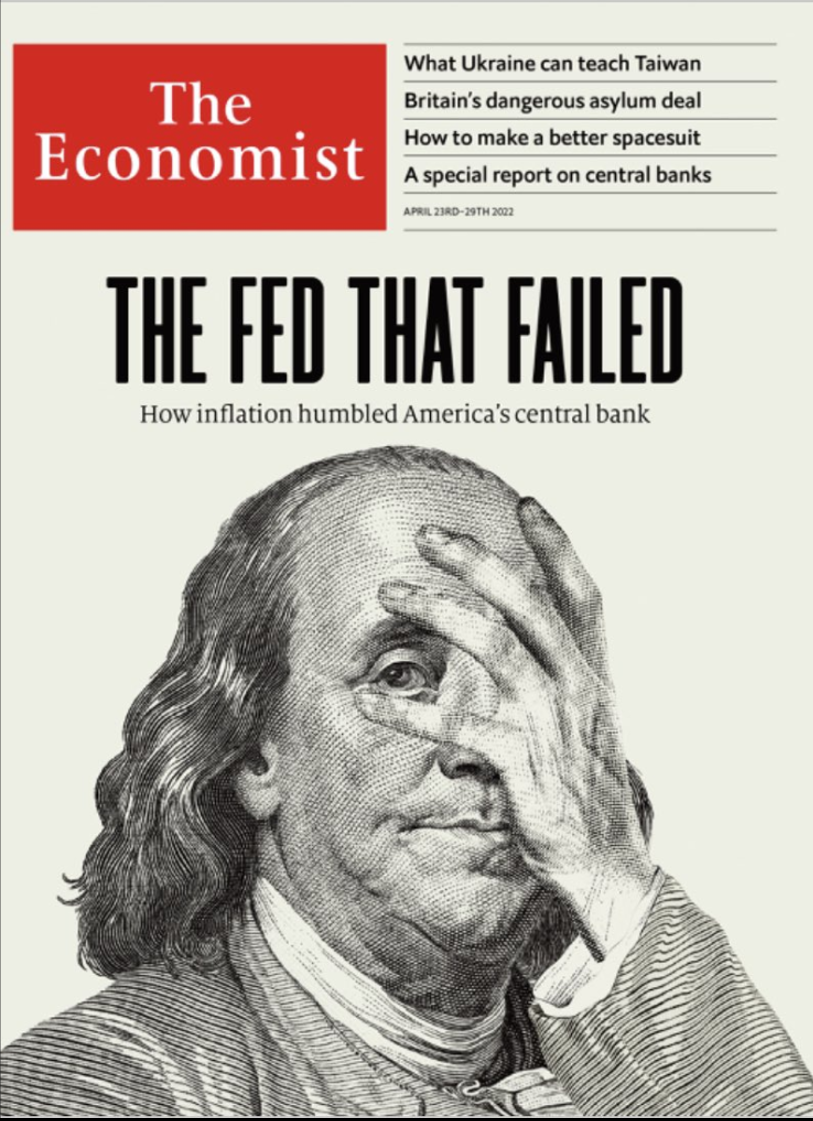

| Here is the front page of the new Economist. Unfortunately, readers will only think the Fed’s failure just occurred because of the current bout of inflation, but their failures have been building for decades and higher inflation is only the kryptonite that has exposed them.

|

| What the Fed has wrought over the decades by playing God over the most important price in capitalism, the cost of capital:

1) With the encouragement of always being there to bail out situations of financial distress, like LTCM, and also quick with the trigger on rate cuts such as after the 1997 Asian crisis, a generation of moral hazard was born.

2) Via ever-falling interest rates, most of which were pushed lower by the Fed, they encouraged a legacy of ever-rising borrowing and debt.

3) Housing has become more and more unaffordable over the past few decades.

4) The U.S. financial system was on the cusp of collapse in 2007-2008, encouraged in the years prior to borrow and speculate in a search for yield in response to artificially placed interest rates.

5) Just a few years prior to that housing boom and bust, Greenspan egged on the tech bubble, which was epic for those that didn’t see it.

6) Congress (both parties) got the green light via the low cost of funding to take us to $30 trillion relative to a $24 trillion economy.

7) All resulting in financial fragility where modest changes in interest rates now have a pronounced impact on everything and the jump in consumer price inflation (following so many years of asset price inflation) now puts the entire system to a major test.

|

.png)