|

| Quality silver assets are scarce.

|

| Finding one in a single project is rare enough. Finding four of them...in the same world-class Mexican silver belt...inside a single small-cap company...is something else entirely.

|

| But that’s just what Kootenay Silver Inc. (KTN.V; KOOYF.OTC) offers right now. And much more.

|

| The company controls no less than four silver deposits across Mexico’s Sonora and Chihuahua states — and all of it anchored by a flagship project that just posted a positive Preliminary Economic Assessment with a $763 million after-tax net present value. (And a rich 41% internal rate of return!)

As you’re about to see, that PEA is only one piece of the story. The other three deposits, including a fast-growing high-grade discovery next door, may matter just as much to how this stock gets valued from here.

|

| A District That’s Been Producing Since The 1650s

|

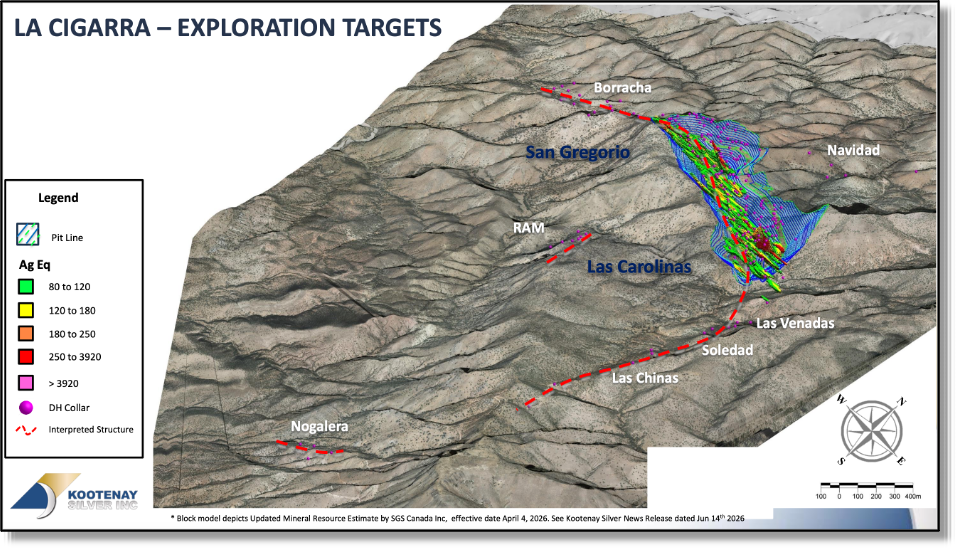

| Kootenay’s La Cigarra project sits within the Parral Mining District of Chihuahua State, a region that has produced silver for over 350 years.

|

| The nearby Santa Barbara and San Francisco del Oro mines, both still active today, have together produced more than 800 million ounces of silver since the 1650s.

|

| La Cigarra sits along that same mineralized trend, 26 kilometers from the historic city of Parral and just 20 kilometers north of the active Santa Barbara and San Francisco del Oro camp.

Good roads, nearby power and an existing experienced local workforce all support a faster path to production than most undeveloped silver projects enjoy.

|

| Zoom out further and La Cigarra sits on the broader Sierra Madre silver trend, the same belt that runs through Fresnillo, Zacatecas and Guanajuato, camps that have each produced over a billion ounces of silver historically.

|

| Columba, profiled below, sits on this same trend. That history explains why this district keeps attracting drill bits four centuries after the first ones went into the ground.

|

| The PEA That Changes Everything...

|

| Released June 15, the La Cigarra PEA outlines a 14-year open-pit operation processing 6,000 tonnes per day, with average silver recovery of 89.3%.

At consensus metal prices of $50.00 per ounce silver, the project delivers a $763 million after-tax NPV and 41% IRR.

That’s great...but the project is also highly leveraged to the price of silver:

|

| At a recent spot silver price of $67.23 per ounce, those numbers jump to almost $1.3 billion in NPV and a 64% IRR.

|

| Initial capital cost is a manageable $332 million. The project is set to produce 63.6 million payable ounces of silver over its life, averaging 6.22 million ounces of annual silver production over the first five years, with a rich $107 million in after-tax revenue per year.

The PEA runs on an updated resource of 60.02 million ounces measured and indicated, plus another 17.25 million ounces inferred.

That resource sits within a six-kilometer mineralized corridor defined by surface mapping and dozens of exploration holes, with the deposit remaining open along a nine-kilometer trend overall. Management has identified exploration potential down-dip, along strike and on parallel structures the current pit design hasn’t even tested yet.

|

| A 10,000-meter drill program targeting the Gap Zone between the deposit’s two main resource areas is set to begin this fall, with the potential to add another 10% to 20% to the pit shell.

|

|

| Kootenay has identified multiple exploration targets in the vicinity of its current proposed pit design that has already provided significant economic results.

|

| In addition to leverage to the silver price, the PEA’s own sensitivity analysis shows what’s at stake if grades improve. Just a 30% increase in head grade alone pushes the project’s pre-tax NPV to just under $2 billion, before any change in the silver price at all.

|

| The High-Grade Engine

|

| While La Cigarra advances toward feasibility, Kootenay’s newest discovery is doing the heavy lifting on growth.

|

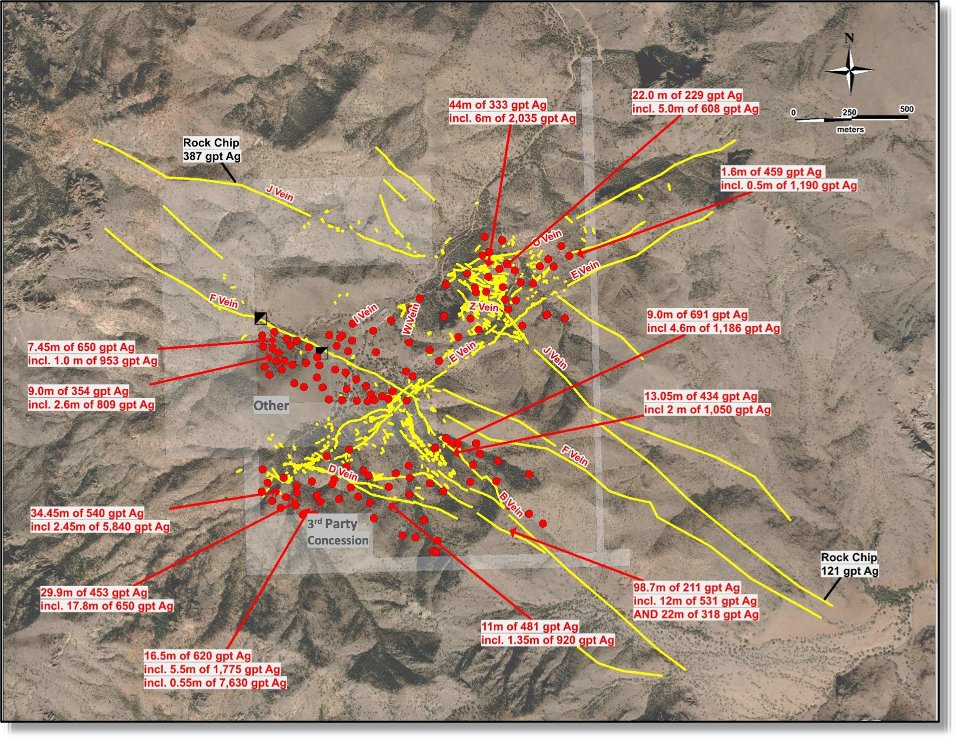

| Columba is a classic high-grade epithermal vein system in Chihuahua State that produced silver briefly in the early 1900s and again in the late 1950s…then sat untouched before Kootenay took it over.

|

| Since 2019, the company has drilled 66,020 meters across 236 holes at Columba. A maiden resource filed in August 2025 already stands at 54.1 million ounces of silver, inferred, grading 284 g/t across 17 separate veins.

|

|

| Kootenay’s Columba project shows a high number of veins that have been and continue to produce exciting – and growing – mineralization.

|

| Recent intercepts support the high-grade nature of this project, including 10 meters of 503 g/t silver on the Lupe Vein, with a high-grade core running 3,620 g/t over 1.10 meters, and 16.5 meters of 620 g/t on the D Vein, including a half-meter interval running 7,630 g/t.

|

| The current 60,000-meter program, expanded from an original 50,000 meters, is broken into specific targets across the vein system.

|

| Consider these upcoming catalysts: The D Vein alone is slated for 22,000 meters across 40 holes testing depth and extension. The B Vein corridor, the F Vein extensions and the J-Z Vein swarm each have dedicated programs, and 10,000 meters are set aside purely for testing veins that haven’t been drilled at all.

With assay results like these flowing on a rolling basis, Columba is positioned to generate a steady stream of news through the rest of 2026, each release a chance to move the resource, and the stock, higher.

|

| Four Deposits...

And One Big Re-Rating Opportunity

|

| Add it all up and Kootenay’s four-deposit portfolio, La Cigarra, Columba, Promontorio and La Negra, hosts an extraordinary 231.8 million ounces of silver-equivalent measured and indicated plus another 118.2 million ounces inferred.

|

| That kind of scale is rare for a company with a market cap of roughly C$135 million.

|

| Here’s the bottom line: At over six million ounces a year of production...plus a pipeline of projects right behind La Cigarra...Kootenay is a prime target for a rich buyout from a major at any time.

|

| And if it doesn’t get bought out, the “downside” is that Kootenay advances this exceptional project itself — and becomes the world’s next mid-tier silver producer!

|

| That’s two paths toward potentially rich payouts for shareholders.

|

| More Than

Twice The Company At Half The Price

|

| Thanks to the vagaries of today’s market, Kootenay has become one of the more remarkable bargains in recent history.

|

| Consider that the company’s shares currently trade at only around half their levels from late January, when silver prices had risen again to all-time highs.

|

| Since then, the company has delivered exactly what the market was waiting on: a completed PEA carrying a $763 million NPV, an upsized C$18 million financing that closed in February and a steady run of high-grade drill results out of Columba.

|

| But what also happened in that time period? The conflict between the U.S. and Iran and the resulting sell-off in risk assets, including metals and mining.

That’s what led the market to essentially overlook the remarkable PEA — showing a valuation many times the company’s entire market cap.

|

| If anything, the company should be valued at much more than it was on the day it hit that January high.

Instead, investors can get the shares at a deep discount to those previous levels.

The recent financing leaves Kootenay funded for the next 18 to 24 months with no need to return to the market. A 10,000-meter drill program targeting the Gap Zone at La Cigarra starts this fall. And Columba’s drill program keeps delivering results, with more on the way.

A positive PEA. A high-grade discovery still growing. A balance sheet built to fund both. Obviously, the time to look into Kootenay Silver is now.

|

| CLICK HERE

To Learn More About Kootenay Silver

|

.png)