|

| When a development-stage gold company owns 8.2 million ounces of gold across two of the largest undeveloped projects in Canada, you would expect the market to notice.

|

| Instead, First Mining Gold (FF.TSX; FFMGF.OTC) has spent years trading like an afterthought, even as gold itself has rocketed to record heights.

|

| That gap between asset value and share price is exactly why this story is worth your attention right now.

|

| As you are about to see, the company just cleared its two biggest speedbumps…and the rest of the value gap may not stay open much longer.

|

| Six Million Ounces…For Free?

|

| The simple math captures a major piece of this story.

First Mining’s market capitalization sits at roughly C$950 million. Its flagship Springpole project alone, the largest of its two core assets, carries an after-tax net present value of $2.1 billion at a base-case gold price of just $3,100/oz.

|

| At today’s spot gold price, that NPV jumps to $3.8 billion.

|

| That means that Springpole alone arguably values First Mining all by itself — meaning that investors get First Mining’s second flagship asset as a bonus.

...And that asset is none other than the six-million-ounce Duparquet gold project in Quebec’s Abitibi Greenstone Belt, one of the most prolific gold-producing regions on earth.

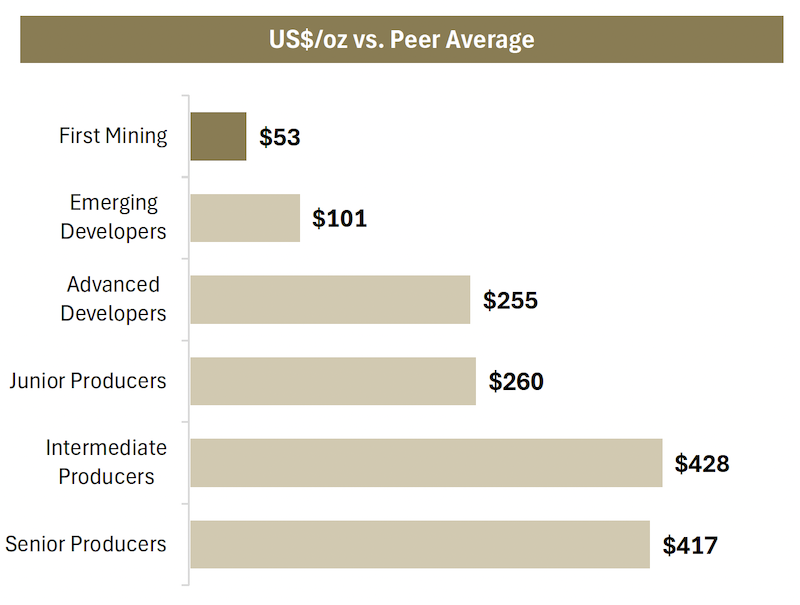

Put another way, First Mining is trading at roughly US$53 per ounce of gold resource, while its peer group of advanced and emerging developers trades at multiples of that figure, with senior producers fetching closer to US$417 per ounce.

|

| |

| Even a modest re-rating toward peer averages would represent a dramatic move higher for First Mining’s share price.

|

| The Overhang Has Just Lifted...

|

| Permitting a major gold mine in Canada is a long, multi-year process, and it’s one of the biggest reasons undeveloped gold projects sit undeveloped for so long.

|

| Most competing projects of this scale are still in the earliest stages of that process. First Mining, by contrast, is already well down the road.

|

| Springpole has just received its federal Environmental Assessment approval, clearing the central regulatory hurdle that gold projects of this scale often spend the better part of a decade navigating.

Alongside that, the local First Nation communities completed their Impact Assessment process for Springpole and authorized the project, with First Mining now working to finalize a binding Springpole Project Agreement.

|

| This is the kind of dual milestone that puts First Mining years ahead of most other undeveloped, multi-million-ounce gold projects in Canada...and one that competitors will have a hard time catching up to anytime soon.

|

| With those overhangs lifting, First Mining is shifting from a story about gold-price optionality to a story about major advancement...and the valuations that brings.

|

| Momentum Building On A Second Front

|

| Springpole isn’t the only project building value here.

|

| Duparquet hosts 3.4 million ounces of gold in the indicated category and 2.6 million ounces inferred, and First Mining’s 2026 drilling campaign is underway right now.

|

| The results from previous drilling are already impressive: Assays from the Miroir target, located along the Valentre trend, include 3.20 g/t gold over 15.75 meters and 2.01 g/t gold over 29.80 meters, continuing to extend mineralization at depth and along strike, with results from the ongoing program still to come.

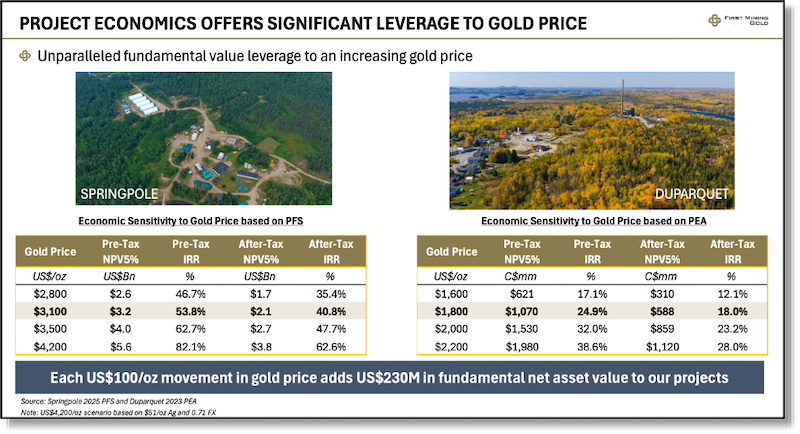

Duparquet’s September 2023 preliminary economic assessment outlined an 11-year mine life, average annual production of 233,000 ounces of gold, and an after-tax NPV of C$588 million at an extremely conservative $1,800/oz gold price.

And Duparquet is massively leveraged to the gold price. Consider that at just $2,200/oz — still well below today’s spot price — that after-tax NPV nearly doubles to C$1.12 billion.

|

| Even More Leverage To Gold

|

| Not only does First Mining boast two world-class resources, it also offers about as much torque to the gold price as you will find anywhere in this market.

According to the company’s own sensitivity analysis, every US$100/oz move in the gold price adds roughly US$230 million in fundamental net asset value across its two flagship projects.

|

|

| Both of First Mining’s projects offer tremendous leverage to the gold price, with billions in added value with realistic price assumptions.

|

| Consider that, at the spot case of US$4,200/oz gold, Springpole’s after-tax NPV alone climbs to US$3.8 billion, nearly four-and-a-half times First Mining’s entire current market capitalization.

|

| And as mentioned before, Duparquet’s after-tax NPV at $2,200/oz already stands at nearly double its $1,800/oz base case.

|

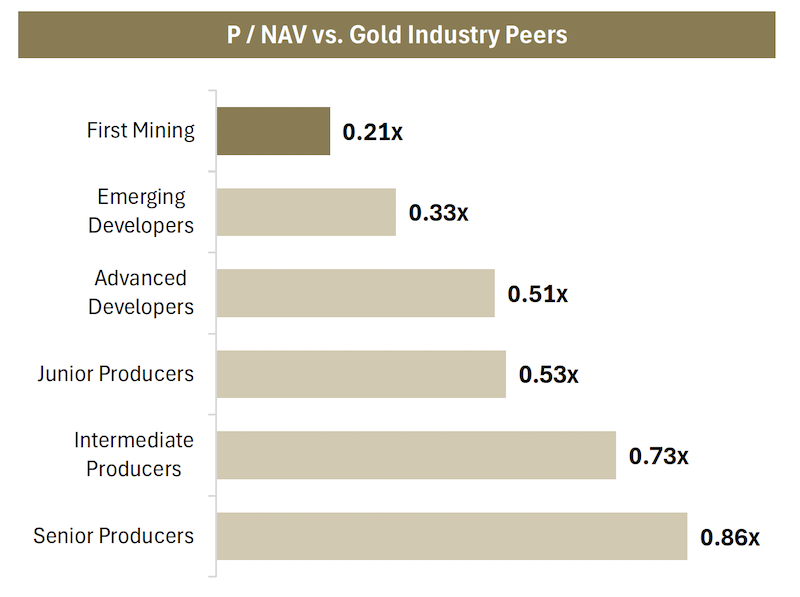

| That leverage cuts both ways on valuation.

First Mining’s own price-to-net-asset-value comparison shows the company trading at just 0.21x NAV, versus an average of 0.51x for advanced developers and as high as .86x for senior producers.

Closing even half that gap implies meaningful upside from current levels.

|

| |

| First Mining’s current price-to-NAV leaves room for potentially exceptional valuation gains as it simply advances along the development track.

|

| A New Set Of Eyes On The Stock

|

| Permitting progress isn’t the only thing changing how this story gets seen in the days just ahead....

You see, First Mining is on track to be added on to the VanEck Junior Gold Miners ETF (GDXJ) in its next re-balancing cycle at the end of August. This is the benchmark index tracked by generalist and institutional gold investors alike.

|

| Index inclusion of this kind often brings a wave of passive buying and a fresh round of institutional attention that a stock simply does not get while sitting outside the major gold indices.

|

| Combined with the Springpole permitting breakthroughs and the upcoming Duparquet drilling results, First Mining now has multiple, overlapping reasons for the market to take a fresh look.

|

| A Story The Market Has Yet To Fully Price In

|

| So when First Mining describes itself as building tomorrow’s gold producer, the evidence backs it up:

|

- Two of Canada’s largest undeveloped gold projects...

- Federal and First Nations approvals now secured at Springpole...

- ...And on track to be added to a major gold index

|

| Why does a company with this much gold, this much progress, and this much leverage to gold still trade at a fraction of its peers’ valuations?

The simplest answer is that the market has been slow to catch up during the recent gold-market volatility.

|

| With permitting risk falling away and a wider pool of index-driven investors now able to own the stock, that gap looks increasingly hard to justify...and ready to close.

|

| The federal approval is in hand. The First Nations agreement is in hand. The drill bit is turning at Duparquet. The leverage to gold prices sits fully intact.

And the time to look into First Mining Gold is now.

|

| CLICK HERE

To Learn More about First Mining Gold Corp.

|

.png)