This has traditionally been a good time of the year to be a gold bug.

|

Vacationing traders and investors put the kids back into school and get back to their desks.

Market volume picks up, and news begins to flow from summer exploration programs.

|

This year, rampant inflation stoked by waves upon waves of government stimulus has greatly increased the odds that this fall will be a strong one for gold.

|

Even a casual glance at gold’s last big jump after the COVID-19 lockdowns last March will show you that gold royalty companies are the first off the shelf when the yellow metal gets into bull mode.

Investors are attracted to gold royalty companies’ low-cost, high-margin operating model and bid up these names early (and explosively) when gold ticks upward.

Lingering worries about the Fed’s response to inflation have kept gold prices muted this summer, which means there are still bargains in the space…for now.

|

One gold royalty play that stands out to maximize leverage on a fall run for gold prices is Vox Royalty (VOX.V; VOXCF.OTC).

|

As you’re about to see, this hard-charging, fast-growing company is just hitting the steep part of its growth curve.

If and when that fall bull run for gold kicks in, owning Vox Royalty beforehand could deliver explosive gains.

|

Fast-Growing Revenues Are

The Tip Of The Iceberg

|

What makes Vox a go-to name in this space?

|

| |

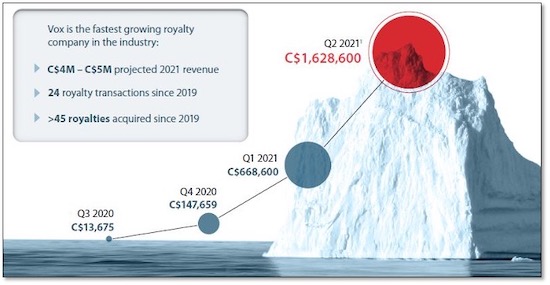

Well, for starters, take a look at the graphic above, which charts Vox’s meteoric rise in revenues — an average of 492% revenue growth over the past four quarters.

|

That level of growth makes Vox the royalty sector’s fastest-growing company in terms of quarterly revenue growth.

|

It’s a level of performance the company expects to continue — it recently doubled its full-year 2021 revenue guidance to between C$4 million and C$5 million.

Driving this impressive level of growth is the great work Vox has done to build both its overall royalty portfolio (currently at 54 royalties) and its stable of producing royalties.

|

|

That latter asset is key, as cash flow is king for a royalty company’s valuation.

Vox’s producing royalties have increased five-fold over the past year.

And the company is just getting warmed up. By 2023, management is forecasting its producing royalty count will double and, by 2026, it could more than triple.

|

|

And that’s just with the royalties Vox currently has on the books. There’s every reason to believe that the company will continue to build out its overall royalty portfolio.

Given the company’s growth prospects, both in terms of current cash flow and producing assets, is it any wonder that brokers from Cantor Fitzgerald, RedCloud and Paradigm Capital have issued “buy” recommendations on Vox Royalty?

Save

Not A Subscriber Yet?

Get Golden Opportunities For Free

Subscribe to our Golden Opportunities e-letter to receive timely market

updates from the Gold Newsletter research team, plus video

presentations by expert speakers from the New Orleans Conference

— and the Investor’s Guide to Gold and Silver — all at no cost!

CLICK HERE to start your subscription.

|

|

Longer term, there’s the very real prospect that Vox will attract the attention of an acquiring company.

That trend in the sector has already started — in June, Gold Royalty Corp. snapped up Ely Gold at more than a 40% premium on its trading price at the time.

|

Cash flow is king, but scale matters as well. If Vox keeps up its current breakneck pace of growth, bigger players looking for scale could eventually make a similar takeout offer for Vox.

|

In the interim, continuing to post revenue growth over the next few quarters could well goose Vox’s share price in the short term…and start drawing the attention of those potential suitors.

|

|

At current trading levels, Vox Royalty is in great position to deliver leverage on fall strength for gold.

Consider the facts:

|

• Vox’s revenues have grown by an average of 492% over the past four quarters…

• Management recently doubled its 2021 revenue guidance to C$4-C$5 million…

• The company’s stable of producing royalties is forecast to double by 2023 and triple by 2026…

• Vox’s unique business model will continue to grow its already large portfolio via acquisition…

• Organic news will continue to flow at a prodigious rate from its near-production royalties, keeping the company top-of-mind among investors in this sector.

Add in Vox’s recent upgrade to the OTC-QX Best Markets board in the U.S. and you have a recipe for potential big price gains in the near future.

|

But with September now upon us, time is short and current bargain price levels may not last long.

|

|

.png)