With all the talk about gold and silver bull markets this year, it can be easy to lose track of the post-Covid-crash rebound the base metals have seen.

|

As dollar-denominated assets, they also benefit from the tsunami of fiscal and monetary stimulus that has rolled through the economy.

And China, the manufacturer to the world and source of the coronavirus, got the pandemic under control early, which has allowed it to return to economic growth.

It’s a conducive environment for a polymetallic metal producer like Sierra Metals (SMTS.NYSE-A; SMT.TO).

Sierra’s three operating mines (one in Peru, two in Mexico) give investors exposure not only to silver and gold, but also to copper, zinc and lead. It’s a veritable one-stop shop for a post-Covid economic rebound.

|

But dig into the story just a bit, and you see an even stronger argument for investing right now.

|

You see, after struggling through a first half that saw shutdowns on both its Yauricocha mine (Peru) and its Bolivar mine (Mexico), Sierra’s production rebounded in the most recent quarter, as those projects were back online for the full period.

Add in renewed production from the Cusi silver mine in Mexico and you have a story that’s hitting its stride…and at the perfect time.

|

Yauricocha:

The Mine That Keeps On Giving

|

Sierra’s Yauricocha mine lies in west-central Peru and has been in operation for an amazing 72 years.

The underground mine has kept on producing over all that time because of the consistent copper-zinc-lead mineralization there.

Sierra took an 82% interest in the mine in 2011 and, due to that consistent mineralization, has been able to maintain seven-to-eight years worth of reserves by steadily drilling off the next areas for mining.

|

|

|

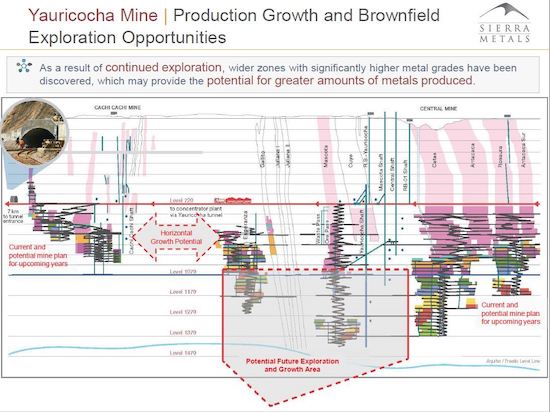

| The gray areas above show how the underground operation at Yauricocha still has plenty of room to grow, in spite of being in operation since 1948. |

As the map of the underground operation shows, the mine has a lot of room left to grow and add reserves from here.

|

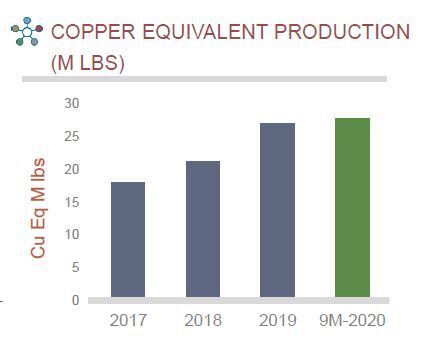

In the meantime, the mine produced 22.2 million copper-equivalent pounds in Q3 2020 and appears on track to produce as much or more copper-equivalent material as it did in 2019.

|

This could happen despite the Covid shutdowns that kept Yauricocha shuttered for part of Q1 and much of Q2.

With all-in sustaining costs for the first half of just $2.05/lb — and with copper prices currently hovering around $3.00/lb — the mine’s financials will likely show significant profitability when Sierra Metals publishes them next month.

|

Bolivar:

A Copper-Intensive Producer With Room To Grow

|

Then you factor in the production from the Bolivar copper-silver-gold mine in Chihuahua State, Mexico.

Also subject to a shutdown in Q2, the mine bounced back strongly in Q3 — producing 10.2 million lbs. of copper-equivalent.

In the first nine months of 2020, despite significant downtime, Bolivar has produced more copper-equivalent (27.8 million lbs.) than in all of 2019 (27.2 million lbs)!

|

|

|

| Sierra Metals’ Bolivar mine has produced more copper-equivalent metal in the first nine months of 2020 than in all of 2019. |

Better still, exploration has identified the Bolivar Northwest and Bolivar West targets that could increase the mill feed and, in some cases the head grade, at the project.

As it stands, Bolivar has reserves of 7.2 million tonnes and resources of 41.0 million tonnes.

So, as you’ll see in a moment, Sierra offers not only short-term gains as it returns to profitability, but also longer-term gains based on production growth.

Save

Not A Subscriber Yet?

Get Golden Opportunities For Free

Subscribe to our Golden Opportunities e-letter to receive timely market

updates from the Gold Newsletter research team, plus video

presentations by expert speakers from the New Orleans Conference

— and the Investor’s Guide to Gold and Silver — all at no cost!

CLICK HERE to start your subscription.

|

Cusi:

Silver Operation Starts To Come Into Its Own

|

But first, there’s one last piece of the company’s production puzzle: its Cusi silver-zinc-lead-gold operation, which is also in Chihuahua State.

The mine boasts a 50-million-ounce silver resource (39.1 million ounces of measured and indicated silver-equivalent and another 10.9 million ounces of inferred silver-equivalent).

The mine struggled in recent years and saw production paused in Q2 2020 and into July. It produced 614,000 oz. silver-equivalent for the first nine months of the year.

The good news here is that silver prices have surged in 2020, and the company has zeroed in on an area of higher-grade material that can help return Cusi to profitability.

|

To make a long story short: Management expects costs that have been in the $20 range to come down to a more manageable $14-$16/ounce range in the near future.

|

Combined with the new silver discovery around Cusi that is seeing 1,000 meters of drilling, there’s real upside here from both exploration and operational improvements.

|

The Upcoming Catalyst:

Q3 Numbers Will Hit The Market In Early November

|

Thus, even in the face of the pandemic, Sierra Metals is very much in a growth phase.

In the short term, the Q3 2020 financial numbers due out soon have a real chance of surprising to the upside, given the quarter’s strong production numbers.

|

But there’s very much a longer-term case for Sierra Metals as well.

|

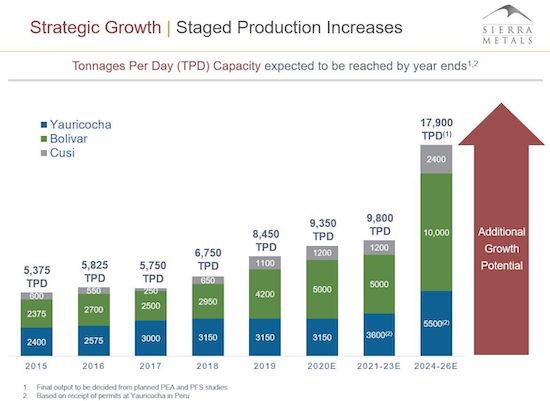

As the graphic below indicates, the growth it has enjoyed from its Yauricocha and Bolivar operations will continue (and likely accelerate) in the years ahead.

|

|

|

| Production from all three of Sierra Metals’ mines could grow substantially in the years ahead. |

|

Sierra is looking at significant cash flow improvements in the back half of this year and into next year.

This should add nicely to the $40 million in cash reserves the company already has on hand. That’s money Sierra can use to continue growing the resources on its projects.

|

With a downside protected by producing assets…and upcoming catalysts for a potentially significant rerating…plus a clear path for growth, Sierra Metals’ risk-reward profile is very much in investors’ favor right now.

|

The Q3 numbers are due out next month, making now a perfect time to build a position in this growth-oriented metals producer.

|

.png)